Many Nigerians work hard every day, yet still find it difficult to save money, invest, pay bills comfortably, or make real financial progress.

From rising food prices and transport costs to family responsibilities, unemployment, and low income, there are many genuine reasons why managing money has become challenging.

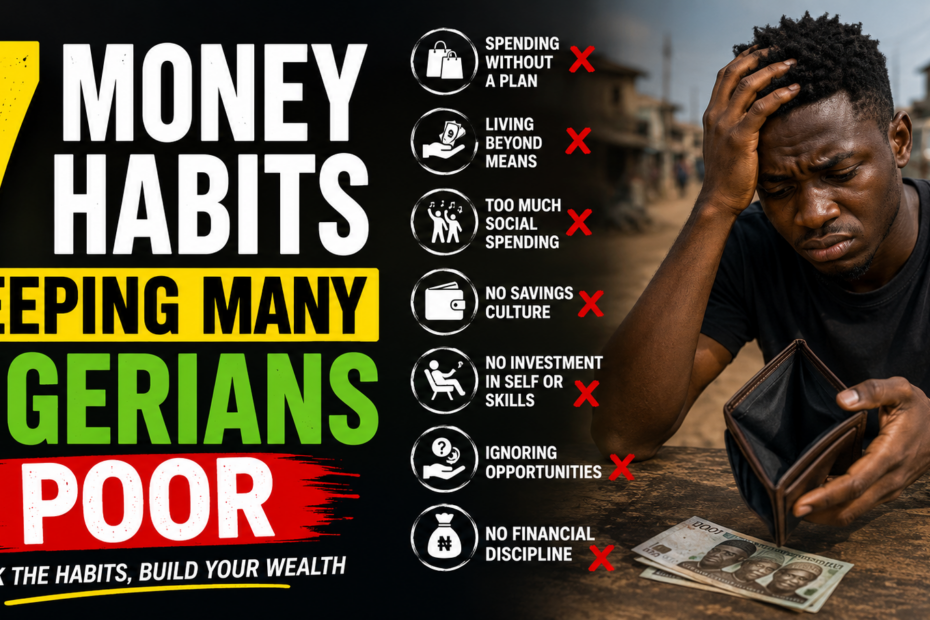

However, financial struggles are not always caused by low income alone. In many cases, certain money habits quietly make the situation worse over time.

Spending without a plan, borrowing for unnecessary things, trying to impress others, and failing to save even small amounts can keep a person trapped in a cycle of financial pressure.

The good news is that money habits can be changed. By identifying and correcting these habits, many Nigerians can begin to take better control of their income and build a more stable financial future.

Here are seven money habits keeping many Nigerians poor.

Trying to Impress People

Another major money habit keeping many Nigerians financially stuck is the pressure to impress other people. In today’s world, especially with social media, there is constant comparison.

Many people feel they must look successful even when their bank account tells a different story. This leads to spending beyond their means on expensive clothes, latest smartphones, parties, weddings, outings, and even cars they cannot comfortably maintain.

The problem is that trying to “look rich” often pushes people deeper into financial struggle. Money that should be used for savings, investment, or building a stable future is instead spent on maintaining appearances.

Some people even borrow money just to attend events or upgrade their lifestyle so they can match what they see online or in their social circle.

It is important to understand that looking rich is not the same as being financially stable. A person may appear successful on the outside but still be living under constant financial pressure behind the scenes. Real financial progress is not about applause or attention; it is about peace of mind, savings, and growing income over time.

Instead of competing with others, it is wiser to focus on personal growth. Building useful skills, increasing income, saving consistently, and investing wisely will always matter more than social validation.

The people who truly achieve financial freedom are often those who stop trying to impress others and start focusing on their own financial journey.

Borrowing for Things That Do Not Make Money

Not Saving Because Income Is Small

One common money habit that keeps many Nigerians financially stagnant is the belief that saving is only for people who earn high incomes.

Because of this mindset, many individuals ignore saving completely, thinking that their salary or daily income is too small to make any difference. Over time, this habit delays financial growth and makes it harder to build stability.

The truth is that saving is not about the amount alone, but about consistency and discipline. Even small amounts like ₦500, ₦1,000, or ₦2,000 saved regularly can gradually grow into something meaningful.

More importantly, the habit of saving trains the mind to prioritize the future instead of spending everything at once. It also creates a small financial cushion that can help during emergencies such as transport issues, medical needs, or unexpected expenses.

A better approach is to “pay yourself first.” This means that whenever money is received, a portion should be set aside for savings before any spending begins.

Even if the amount is small, it should be treated as important and non-negotiable. After saving, the remaining money can then be used for daily needs and responsibilities.

Over time, this simple discipline builds financial confidence. It teaches control, reduces dependency on borrowing, and slowly prepares a person for bigger financial opportunities like investing or starting a small business. :::

Depending on Only One Source of Income

Relying on only one source of income is another habit that quietly keeps many Nigerians financially vulnerable. Whether it is a monthly salary or a single small business, depending on one stream of income can be risky, especially in an economy where job security is not always guaranteed and the cost of living continues to rise.

When that single income is affected—through job loss, reduced sales, or unexpected delays—financial pressure can become immediate and overwhelming.

Having only one income source also limits how fast a person can grow financially. Even if someone manages their money well, there is only so much they can save or invest from one stream. This is why exploring additional, realistic income opportunities is very important for long-term stability.

There are many practical options Nigerians can consider based on their skills and environment.

These include freelancing, tutoring students, selling products online, content writing, digital services like graphic design or social media management, farming on a small scale, operating a POS business, delivery services, or learning a valuable skill that can be monetized over time.

The key is to start small and grow gradually, not to rush into everything at once.

However, it is important to be careful and avoid scams or get-rich-quick schemes that promise unrealistic returns. Many people lose money chasing shortcuts instead of building real skills or businesses. True financial progress comes from steady effort, patience, and consistency.

The goal is not to abandon a main job or business, but to slowly build additional streams of income that can support and strengthen financial stability over time.

Ignoring Financial Knowledge

Another money habit that quietly keeps many Nigerians financially stuck is ignoring financial knowledge. Many people focus only on earning money but rarely take time to understand how money actually works.

As a result, they may work for many years without learning basic principles of budgeting, saving, investing, debt management, or how to grow income over time.

When financial knowledge is missing, it becomes easy to make repeated mistakes such as overspending, taking bad loans, or falling for poor investment decisions.

Without understanding how money grows, a person may always depend on salary or daily income without building anything long-term. This limits financial progress, even if income increases over time.

The good news is that financial education is more accessible today than ever before. People can learn through books, trusted finance blogs, podcasts, online courses, seminars, and advice from experienced professionals. Even small consistent learning can gradually change how a person thinks about and handles money.

However, it is also important to be careful with information from social media. Not every advice is reliable, especially when it comes to investment opportunities that promise fast or unrealistic returns.

Many financial scams are designed to look attractive by guaranteeing quick profit with little or no risk. A healthy financial mindset requires patience, research, and skepticism toward anything that sounds too good to be true.

Improving financial knowledge does not require becoming an expert overnight. It starts with small learning habits that help a person make better decisions with their money. Over time, this knowledge becomes one of the strongest tools for building financial stability and avoiding costly mistakes.

Spending Every Increase in Income

One money habit that quietly prevents many Nigerians from building real wealth is the tendency to spend every increase in income.

When people start earning more money, instead of improving their financial stability, they often upgrade their lifestyle immediately.

This can include moving to a more expensive apartment, buying more expensive clothes and gadgets, eating out more frequently, or taking on financial responsibilities that match their new income level.

While it feels rewarding to enjoy a better lifestyle, the problem begins when spending rises at the same rate as income. In that situation, there is no real financial progress, even though earnings have increased. The person may look more comfortable on the outside but remain financially vulnerable on the inside.

A simple example is someone earning ₦50,000 monthly who spends almost all of it. If their income increases to ₦150,000, but their spending also increases to ₦150,000, their financial situation does not actually improve.

They are still living paycheck to paycheck, only at a higher level. There is still no savings, no emergency fund, and no investment for the future.

True financial growth happens when income increases are used to improve financial habits, not just lifestyle. A portion of any income increase should go into savings, investments, and building an emergency fund. This creates financial breathing space and reduces dependence on constant income flow.

Instead of upgrading lifestyle immediately, it is wiser to first upgrade financial security. Over time, disciplined use of increased income leads to stability, freedom from debt pressure, and the ability to handle unexpected financial challenges with confidence.

Conclusion

In conclusion, becoming financially stable is not something that happens overnight, especially in a challenging economy like Nigeria where many people are already dealing with rising costs and limited income.

However, the good news is that financial progress is possible when small but consistent money habits are changed over time. The way a person handles money matters just as much as how much they earn.

Instead of trying to change everything at once, it is wiser to start with one simple step.

This could be tracking daily expenses, creating a basic budget, saving a small amount every week, avoiding unnecessary debt, or learning a profitable skill that can increase income. Each of these actions may seem small, but they build strong financial discipline over time.

With patience, consistency, and better financial decisions, anyone can gradually reduce money pressure and move toward a more stable and secure financial future.

Frequently Asked Questions

What Is the 7-7-7 Rule for Money?

The 7-7-7 rule for money is a simple personal finance guideline that helps people manage income in a balanced and disciplined way.

While different financial coaches may explain it slightly differently, the idea is generally centered around dividing your income into three major parts of 70%, 20%, and 10%, sometimes expanded into a more detailed structure that still follows a “seven-based” mental model for easy remembering.

The goal is to create a system where money is not only spent but also saved and invested consistently.

In a practical sense, the largest portion is usually used for essential living expenses such as food, transport, rent, and daily needs.

The second portion is directed toward savings or emergency funds, while the final portion is focused on investments, debt repayment, or wealth-building activities.

The strength of this rule is not in the exact numbers but in the discipline it creates. Many people struggle financially not because they do not earn enough, but because they lack structure in how they manage what they earn.

For Nigerians and people in similar economies, this rule can be very useful because it helps control lifestyle inflation. Instead of spending every increase in income, the rule forces you to allocate money intentionally.

Over time, this builds financial stability, reduces stress, and creates a habit of long-term thinking rather than short-term survival.

What Habits Keep People Poor?

One of the strongest habits that keeps people financially stagnant is living without a clear budget or financial plan.

When money is spent impulsively without direction, it becomes very difficult to track where income goes, and this often leads to constant shortage before the next income arrives.

Another major habit is lifestyle inflation, where people increase their spending immediately after earning more money instead of saving or investing the extra income.

Another damaging habit is relying heavily on debt for consumption rather than productive purposes.

Borrowing money to fund unnecessary expenses creates a cycle where a large portion of future income is already committed before it is even earned.

Poor saving culture also contributes significantly, as many people delay saving until “there is extra money,” which rarely happens consistently.

In addition, avoiding skill development or refusing to learn new income-generating abilities can also keep people financially stuck.

In today’s economy, income growth is closely tied to skills, and those who do not upgrade themselves often remain in the same financial position for years. Emotional spending, peer pressure, and lack of financial education also play major roles.

What Are 7 Ways to Save Money?

Saving money effectively requires both discipline and structure. One of the most practical ways is to automate savings, where a fixed amount is set aside immediately after income is received.

This removes the temptation to spend first and save later. Another effective method is budgeting, which helps you assign every naira a purpose so that unnecessary spending is reduced.

Cutting down on impulse purchases is another powerful strategy. Many financial losses come from unplanned spending driven by emotions rather than real needs.

Cooking at home instead of eating out frequently can also save a significant amount over time, especially in urban environments. Tracking expenses regularly is equally important because what gets measured gets managed.

Another strong method is setting clear financial goals, such as saving for rent, business capital, or emergencies. When there is a purpose attached to saving, it becomes easier to stay consistent.

Reducing debt and avoiding high-interest loans also helps because interest payments slowly drain income. Finally, increasing income through side skills or small businesses makes saving easier because pressure on limited income is reduced.

What Are the 7 Habits of Billionaires?

Billionaires often share certain behavioral patterns that contribute to their financial success, even though their paths may differ.

One common habit is long-term thinking. They focus on building systems and investments that grow over years rather than chasing quick money.

Another habit is continuous learning, where they consistently study markets, industries, and new opportunities to stay ahead.

Risk management is also a key habit. Billionaires do not avoid risk entirely, but they calculate it carefully and ensure potential losses are controlled.

They also practice discipline in spending, often living below their means despite having significant wealth. This allows them to reinvest more into income-generating assets.

Networking is another strong habit, as they intentionally build relationships with other successful and influential people. Time management is also critical; they prioritize high-value activities and delegate tasks that do not require their direct attention.

Lastly, they are highly focused on value creation, always looking for problems to solve at scale, because wealth is often a result of solving valuable problems.

What Are the 7 Daily Habits?

Daily habits that shape success usually revolve around discipline, structure, and consistency.

One important habit is waking up early, which gives more time for planning and productive work. Another is setting daily goals, which helps provide direction and prevents wasted time.

Reading or learning something new daily is also a powerful habit because it ensures continuous personal growth. Staying physically active, even through simple exercise or walking, helps maintain energy and mental clarity. Planning the day ahead or reviewing tasks is another habit that improves productivity and reduces confusion.

Practicing gratitude or reflection is also important, as it helps maintain emotional balance and reduces stress. Finally, limiting distractions such as excessive social media use allows individuals to focus better on meaningful tasks.

Over time, these daily habits compound and significantly influence financial success, discipline, and overall life direction.

What Are the 7 Types of Poverty?

Poverty is not only about lack of money; it is a broader condition that affects different areas of human life, and understanding its types helps explain why some people remain trapped in it even when opportunities exist.

One major form is financial poverty, which refers to insufficient income to meet basic needs such as food, shelter, and healthcare. This is the most visible form and often what people first think of when poverty is mentioned.

Another type is educational poverty, where individuals lack access to quality education or skills development. This limits their ability to compete in the job market or create income opportunities.

Closely related is health poverty, which occurs when people cannot access proper medical care, leading to poor productivity and reduced quality of life.

There is also opportunity poverty, where individuals are surrounded by limited job or business opportunities, often due to location, environment, or lack of networks.

Mindset poverty is another critical type, where people hold limiting beliefs about money, success, or their own abilities, which prevents them from taking productive action.

In addition, social poverty refers to isolation or lack of supportive relationships and networks that can provide guidance, mentorship, or financial help.

Finally, time poverty affects individuals who are constantly overworked or poorly managed in their time, leaving no space to improve their situation or build long-term wealth.

Together, these forms of poverty show that escaping poverty requires more than money; it requires education, mindset change, opportunity access, and structured life improvement.

What Are the 7 Pillars of Wealth?

Wealth is not built randomly; it is usually supported by strong foundational principles that guide financial decisions over time.

One important pillar is income generation, which focuses on creating consistent and growing sources of money, whether through employment, business, or multiple income streams. Without income, wealth cannot begin.

Another pillar is saving discipline, which involves consistently setting aside a portion of income regardless of amount earned.

This builds financial security and prepares for future opportunities or emergencies. Closely related is investment, where saved money is put into assets such as businesses, stocks, real estate, or other value-generating ventures that grow over time.

Financial education is another key pillar because understanding how money works helps individuals avoid mistakes and make informed decisions. Without knowledge, wealth can easily be lost even after being earned.

Debt management also plays a major role, as controlling unnecessary borrowing prevents financial pressure and protects long-term stability.

The sixth pillar is risk management, which involves protecting wealth through insurance, diversification, and careful decision-making to avoid major financial losses.

Finally, mindset and discipline serve as the foundation of all other pillars. A strong wealth mindset encourages patience, consistency, and long-term thinking, which are essential for sustained financial growth.

What Are the 7 Habits of Highly Successful People?

Highly successful people often share behavioral patterns that consistently support their growth and achievements. One major habit is goal setting, where they clearly define what they want and break it into actionable steps.

This gives direction and prevents wasted effort. Another habit is prioritization, where they focus on tasks that bring the highest value instead of being distracted by less important activities.

Continuous learning is also a key habit, as successful individuals constantly seek new knowledge, skills, and insights to stay competitive.

They also practice self-discipline, which allows them to stay committed to their goals even when motivation is low. This discipline often separates them from average performers.

Another important habit is effective time management, where they plan their days carefully and avoid unnecessary distractions.

They also engage in network building, surrounding themselves with like-minded and successful individuals who can provide opportunities, ideas, and support.

Lastly, successful people practice reflection and self-improvement, regularly reviewing their progress and adjusting their strategies when needed. This habit ensures they do not repeat mistakes and continue improving over time.

What Habits Make You Rich?

Wealth-building habits are usually simple but require consistency over long periods. One of the most important habits is paying yourself first, which means saving or investing before spending on anything else. This ensures that wealth accumulation happens automatically rather than accidentally.

Another powerful habit is living below your means, where you intentionally spend less than you earn regardless of income level.

This creates financial breathing space and allows for consistent savings and investments. Avoiding impulsive spending is also crucial, as emotional purchases often destroy financial plans.

Successful wealth builders also develop the habit of investing early and consistently, even with small amounts, because time and compounding play a major role in wealth creation.

Another important habit is building multiple income streams, which reduces dependence on a single source of income and increases financial stability.

They also focus on learning financial skills, such as budgeting, investing, and business management.

Finally, discipline and patience are essential habits because wealth rarely happens quickly; it is built steadily over time through consistent action and delayed gratification.

What Are the 7 Secrets of Wealth?

Wealth creation often appears complex, but it is built on a few core principles that successful individuals consistently apply.

One major secret is consistency, because small financial actions repeated over time produce large results.

Another is long-term thinking, where decisions are made based on future benefits rather than immediate pleasure.

A third secret is multiple income streams, as relying on one source of income limits financial growth and increases risk.

Another important principle is control over expenses, where wealthy individuals focus on needs rather than unnecessary wants.

The fifth secret is leveraging money, meaning using money to create more money through investments, businesses, or assets instead of leaving it idle.

The sixth is continuous self-improvement, where individuals invest in skills and knowledge that increase earning potential over time.

Finally, the seventh secret is discipline in execution, because ideas alone do not create wealth—consistent action does.

People who build wealth are those who apply what they know without delay or excuses, allowing time and discipline to multiply their financial progress.

What Are 5 Habits That Can Destroy My Life?

Certain habits may look harmless at first, but over time they can seriously damage your financial stability, relationships, and overall direction in life.

One of the most destructive habits is procrastination, which delays important actions and causes missed opportunities.

When people constantly postpone decisions about saving, learning a skill, or starting a business, they often remain stuck in the same position for years while others move ahead.

Another damaging habit is poor money management, especially spending more than you earn. This creates a cycle of debt and financial pressure that becomes harder to escape with time.

Closely related is addiction to instant gratification, where individuals prioritize short-term pleasure over long-term growth. This could involve excessive spending, gambling, or uncontrolled lifestyle habits that drain resources quickly.

A fourth habit is negative thinking and self-doubt, which weakens confidence and prevents people from taking necessary risks or trying new opportunities.

Over time, this mindset limits personal and financial growth. Finally, bad company and peer pressure can also destroy life direction, as the people you associate with often influence your habits, decisions, and financial behavior.

Staying in environments that encourage irresponsibility can keep someone trapped in the same cycle of failure.

What Is the 3 6 9 Rule of Money?

The 3-6-9 rule of money is a simple financial structure that helps people organize their income in a disciplined and strategic way.

While interpretations may vary, the concept generally focuses on dividing money into structured time-based financial goals that improve stability and growth.

The “3” often represents building a 3-month emergency fund, which acts as a basic financial cushion for unexpected situations like job loss or urgent expenses.

The “6” typically refers to building a 6-month financial safety buffer or savings goal, which provides stronger security and reduces dependence on debt during difficult periods.

This stage encourages stronger financial discipline and helps individuals feel more stable in uncertain economic conditions.

The “9” is often associated with long-term financial planning, such as investing for 9 months and beyond or building assets that generate future income.

The strength of this rule lies in its simplicity. It guides people to think beyond daily survival and focus on structured financial stages.

Instead of spending impulsively, individuals are encouraged to build layers of financial protection and long-term growth.

In real-life application, it helps people gradually move from financial insecurity to stability and eventually to wealth-building through consistent planning and discipline.

What Are the 7 Money Rules?

Money rules are basic principles that help individuals maintain financial discipline and avoid common mistakes.

One important rule is always spend less than you earn, because wealth starts with controlling expenses. Without this rule, financial progress becomes very difficult regardless of income level.

Another rule is save before you spend, which encourages setting aside money immediately after income is received.

Closely related is avoid unnecessary debt, especially debt used for consumption rather than productive investment. Debt should only be taken when it can generate value or income.

A fourth rule is always have an emergency fund, which protects you from financial shocks and prevents reliance on loans during crises.

Another important principle is invest consistently, even with small amounts, because wealth grows over time through compounding and patience.

The sixth rule is track your money, as you cannot manage what you do not measure. Knowing where your money goes helps you correct bad spending habits.

Finally, the seventh rule is increase your income streams, because relying on one source of income is risky and limits financial growth. Multiple income sources provide stability and faster wealth building.

What Are the 6 Laws of Wealth?

The laws of wealth are guiding principles that explain how financial success is built and sustained over time.

One important law is the law of income creation, which states that wealth begins with generating value through work, business, or services. Without income, there is no foundation for wealth.

Another law is the law of saving, which emphasizes that a portion of income must always be preserved instead of being fully spent.

Closely related is the law of investment, which shows that money grows when it is put into productive assets rather than being kept idle.

The fourth law is the law of compounding, which means small, consistent financial actions grow significantly over time when left to accumulate.

The fifth is the law of discipline, which highlights that financial success depends on consistency and self-control in spending, saving, and investing.

Finally, the sixth law is the law of value creation, which states that wealth is directly connected to the value you provide to others.

The more valuable your skills, business, or solutions are, the more financial rewards you can attract. Together, these laws show that wealth is not accidental but the result of structured habits and long-term thinking.

How to Become Rich Fast in Life?

Becoming rich quickly is often misunderstood, because real wealth usually takes time to build, even though it can accelerate with the right strategies.

One of the most realistic ways to increase wealth faster is by focusing on high-income skills, such as digital marketing, tech skills, sales, or business development. These skills increase earning power significantly compared to low-income jobs.

Another important factor is starting a scalable business, where income is not limited by time alone.

Businesses that solve real problems or serve large markets have higher potential for rapid growth. Investing early and wisely also plays a role, especially in assets that appreciate or generate passive income over time.

Reducing unnecessary expenses is another way to accelerate wealth building, because money saved can be redirected into investments or business opportunities.

In addition, building multiple income streams increases cash flow and reduces financial dependence on one source.

However, it is important to understand that “fast wealth” still requires discipline, patience, and consistency. Many people fail because they chase shortcuts instead of building strong financial foundations.

True financial growth happens when income increases, expenses are controlled, and money is consistently invested into productive opportunities over time.