Student life in Nigeria can be exciting, but it also comes with serious financial challenges. Most students rely on limited allowances from parents or guardians, and in some cases, small side incomes that are not always stable. At the same time, the cost of basic needs like food, transportation, data, and school materials continues to rise, making it difficult to manage money effectively.

Because of these realities, many students struggle with money management in school. It is very common for a student to receive their allowance at the beginning of the month and find themselves broke within a short period of time. This usually happens not because the money is enough, but because there is no proper plan for how it should be spent.

Without financial structure, small daily expenses add up quickly. Unplanned spending, social activities, and lack of budgeting often lead to students running out of money before the next allowance arrives. This creates stress, dependency, and sometimes unnecessary borrowing just to survive.

This is why budgeting is not just a financial habit for students—it is a survival skill. Learning how to plan, track, and control spending helps students manage their limited resources more effectively. With a simple budget, even small amounts of money can last longer and be used more wisely.

In this guide, you will learn a step-by-step budgeting approach designed specifically for students in Nigeria, helping you stay financially stable throughout your school life.

Why Students Need a Budget

Students in Nigeria face unique financial challenges that make budgeting very important for everyday survival and stability.

One major reason is limited income, as most students rely on allowances from parents or guardians, while some depend on small part-time jobs or side hustles. This income is usually fixed or irregular, meaning it must be carefully managed to last throughout the month or semester.

At the same time, students deal with high costs of feeding, transport, and data. Daily expenses like meals, commuting to lectures, internet subscriptions, and academic materials can quickly add up. Without proper planning, these costs can consume all available money faster than expected.

Budgeting also helps students avoid unnecessary spending and debt. Many students spend impulsively on outings, entertainment, or non-essential items, which leads to financial stress before the next allowance arrives. In some cases, this can even result in borrowing money to survive, creating avoidable debt at an early stage of life.

In simple terms, budgeting gives students control over limited resources. It helps them prioritize essential needs, manage spending wisely, and reduce financial stress throughout their academic journey.

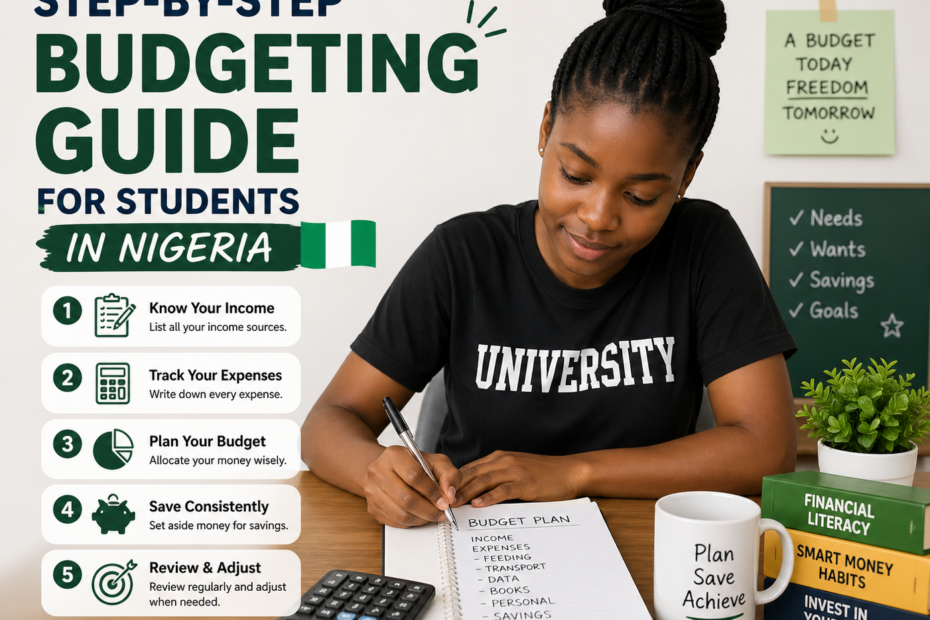

Step 1: Identify Your Total Income

The first step in creating a student budget is to clearly understand how much money you actually receive. Many students struggle financially not because they have no money, but because they don’t properly track or understand their total income.

Start with your pocket money from parents or guardians. This is usually the main and most consistent source of income for most students in Nigeria, so it should form the base of your budget.

Next, include any side hustle or freelance income. This could come from small jobs like tutoring, selling items, online work, or any skill-based earnings. Even if it is not regular, it should still be counted so you can plan realistically.

You should also add gifts or irregular income. This includes money received during holidays, birthdays, or unexpected support from family and friends. While it may not happen every month, it still contributes to your overall financial situation.

In simple terms, this step is about combining all your income sources to know your real earning power as a student. Once you have a clear total, it becomes much easier to plan your spending, avoid overspending, and create a realistic budget that works in your daily school life.

Step 2: List Your Student Expenses

After identifying your total income, the next step is to clearly outline all your expenses as a student. This helps you understand where your money goes and prevents unnecessary spending.

Start with feeding. This is one of the most important daily expenses for students. It includes breakfast, lunch, dinner, snacks, and any occasional eating out. Because it happens every day, feeding often takes a large portion of a student’s budget if not properly controlled.

Next is accommodation. This may include hostel fees, rent, or any housing-related payments. For students living off-campus, this can also include shared utility costs like electricity or water.

Then consider transport. This covers daily movement to lectures, outings, or errands. Whether you use buses, bikes, or ride-sharing services, transport costs can quickly add up if not planned properly.

You should also include data and airtime. In today’s academic environment, internet access is essential for assignments, research, communication, and online learning. However, without limits, data spending can become expensive.

Finally, list academic materials. This includes textbooks, handouts, printing costs, stationery, and other school-related resources needed for your studies.

In simple terms, listing your expenses helps you see the full picture of your spending habits. It makes it easier to plan your budget properly and ensures that your essential student needs are always covered first.

Step 3: Separate Needs vs Wants

Once you know your income and expenses, the next step is learning how to classify your spending. This helps you control your money better and avoid wasting it on things that are not important.

Start with needs, which are the essential things you must spend on to survive and succeed as a student. These include food, school-related needs like textbooks and printing, transport to lectures, and basic living requirements. If these are not covered, daily life and academic performance become difficult.

Next are wants, which are things that improve comfort or enjoyment but are not essential. These include outings with friends, gadgets, fashion items, entertainment, and other lifestyle-related spending. While wants are not bad, they should be controlled carefully, especially when money is limited.

The goal is not to eliminate wants completely, but to make sure they do not come before your needs or affect your ability to manage essential expenses. Many students struggle financially because they spend too much on wants without realizing how quickly it reduces their available money.

In simple terms, separating needs from wants helps you make smarter financial decisions. It gives you control over your spending and ensures that your limited income is used first for what truly matters.

Step 4: Set a Simple Student Budget Plan

After separating your needs and wants, the next step is to turn that information into a clear spending plan. This is where you decide how much money goes to each category so your income is properly organized and controlled.

Start by allocating money per category based on your total income. For example, you can assign specific amounts for feeding, transport, data, school materials, and savings. The idea is to make sure every naira has a purpose so you don’t spend randomly throughout the month.

It is also very important to keep your budget realistic for Nigerian students. Many students fail at budgeting because they set unrealistic limits that do not match actual prices of food, transport, or data. Your budget should reflect real-life costs on your campus or environment, not wishful thinking.

A simple student budget should prioritize needs first, then allow a small amount for wants, and finally include even a small savings portion if possible. Even if the amounts are small, the structure helps you stay in control of your money.

In simple terms, a budget plan is your personal guide for spending. It helps you avoid overspending, manage limited allowance properly, and make sure your money lasts throughout the month or semester.

Step 5: Track Daily or Weekly Spending

Creating a budget is only effective when you also monitor how you actually spend your money. Tracking your expenses helps you stay disciplined and understand whether you are following your plan or going off track.

You can do this using a simple notebook or mobile apps. Write down everything you spend, no matter how small. This includes feeding, transport, airtime, data, and even minor purchases. The goal is not perfection, but consistency in recording your spending.

As you track your expenses, you will begin to identify wasteful spending habits. These are unnecessary costs that slowly reduce your money without you noticing. For students, this may include frequent snacks, unplanned outings, impulse buying, or overspending on data and entertainment.

Once you recognize these patterns, it becomes easier to make better financial decisions. You can reduce or remove unnecessary expenses and redirect that money toward more important needs or savings.

In simple terms, tracking your spending helps you stay aware and in control. It shows you exactly where your money is going and helps you improve your budgeting habits over time.

Step 6: Learn How to Save as a Student

Saving money as a student may seem difficult, especially with limited allowance, but it is still possible if you start small and stay consistent. The goal is not to save large amounts, but to build a habit of saving regularly.

Begin with a small savings habit, such as ₦100–₦1,000 daily or weekly, depending on what you can afford. Even small amounts add up over time and help you develop discipline with money. The most important thing is consistency, not the size of the amount.

You should also aim to build an emergency student fund. This is money set aside for unexpected situations like sudden transport issues, medical needs, or urgent school expenses. Having even a small emergency fund helps you avoid borrowing money from friends or going into debt.

To make saving easier, you can use financial apps like PiggyVest or Kuda. These apps allow you to automate savings, lock funds, and track your progress, which helps you stay disciplined even when temptations to spend arise.

In simple terms, learning how to save as a student is about building consistency early. Small savings today can grow into financial security tomorrow, even with limited income.

Step 7: Avoid Common Student Money Mistakes

Even with a good budget plan, many students still struggle financially because of simple but avoidable mistakes. Recognizing these habits early can help you manage your money better throughout school.

One major mistake is overspending on outings. Social life is an important part of student life, but frequent hangouts, parties, and unnecessary entertainment can quickly drain your allowance. When spending on outings is not controlled, it often affects essential needs like feeding and transport.

Another common issue is no budget tracking. Some students create a budget but never monitor their actual spending. Without tracking, it becomes easy to lose control of expenses and overspend without realizing it. Budgeting only works when you follow it consistently.

A third mistake is spending allowance immediately after receiving it. Many students rush to spend money as soon as it arrives, without planning for the rest of the month. This leads to running out of money early and struggling before the next allowance comes in.

In simple terms, avoiding these mistakes helps you stay financially stable as a student. When you control lifestyle spending, track your expenses, and plan before spending, your money lasts longer and works better for your needs.

Conclusion

Budgeting is one of the most important financial skills every student in Nigeria should learn. It helps you take control of limited income, manage daily expenses wisely, and reduce unnecessary financial stress throughout your school life.

The key lesson is that discipline matters more than income. Even with small allowance, a disciplined student who follows a budget can manage money better than someone with a larger income who spends without planning. Financial success in school is not about how much you have, but how well you manage it.

By learning to plan, track, and control your spending, you give yourself the ability to survive financially and avoid constant money struggles as a student. These habits also prepare you for life after school, where financial responsibilities become even bigger.

Now it’s time to take action. Don’t just read and move on—start practicing immediately. Your challenge is simple: track your spending for 7 days and observe where your money actually goes. This small step will help you understand your habits and improve your budgeting skills significantly.

Frequently Asked Questions

How to start budgeting as a student?

Starting a budget as a student is one of the smartest financial habits you can build early. The first step is to identify your sources of income, such as allowances, part-time jobs, or support from family. Knowing how much money you receive regularly helps you plan effectively.

Next, list your essential expenses. For students, this may include food, transport, data subscription, books, and school-related costs. These should always come first before spending on anything else.

After covering essentials, allocate money for savings, even if it is small. Saving ₦500–₦1,000 regularly builds discipline and prepares you for emergencies.

Then, set a limit for wants, such as entertainment, outings, or shopping. This prevents overspending and helps you stay within your means.

A simple method like the 50/30/20 rule can work well for students, but you can adjust it based on your income. Most importantly, track your spending daily using a notebook or mobile app.

Budgeting as a student is not about restriction—it is about learning control. Starting early gives you a strong financial foundation for the future.

What are the 7 steps in the budget process?

The budgeting process follows a structured approach to ensure effective financial planning. The first step is setting financial goals. This could be saving for rent, starting a business, or building an emergency fund.

The second step is identifying your income sources. This includes salary, side hustles, or any other earnings. Knowing your total income helps you plan realistically.

The third step is listing all expenses. This includes both fixed expenses (rent, utilities) and variable expenses (food, transport).

The fourth step is categorizing and prioritizing expenses. Essentials come first, followed by savings and then non-essential spending.

The fifth step is creating the budget plan. This is where you assign specific amounts to each category based on your income.

The sixth step is tracking your spending. This helps you ensure that you are following your budget and not overspending.

The final step is reviewing and adjusting the budget regularly. Since income and expenses can change, your budget should be flexible and updated when necessary.

Following these steps helps you stay organized and in control of your finances.

What is the 50 30 20 rule for teens?

The 50/30/20 rule for teens is a simple budgeting system that helps young people manage money wisely. It divides income into three parts to create balance between spending and saving.

The first 50% is for needs. For teens, this may include school supplies, transport, or basic personal items. Even if parents cover most expenses, this category helps teens learn responsibility.

The next 30% is for wants. This includes entertainment, games, outings, clothes, or hobbies. It allows teens to enjoy their money without overspending.

The final 20% is for savings. This can go into a savings account for future goals like gadgets, education, or emergencies. Learning to save early builds strong financial discipline.

This rule is effective for teens because it is simple and easy to follow. It teaches them how to balance enjoyment with responsibility.

Over time, teens who use this method develop better money habits and become more financially independent as they grow older.

What is the 70-10-10-10 budget rule?

The 70-10-10-10 budget rule is a structured way of managing income by dividing it into four categories. It helps ensure that money is balanced across spending, saving, investing, and giving.

The first 70% is used for living expenses such as rent, food, transport, and utilities. This covers everyday needs and basic lifestyle costs.

The next 10% is for savings. This includes building an emergency fund or saving for short-term goals.

Another 10% is allocated to investments or debt repayment. This helps grow your money or reduce financial obligations over time.

The final 10% is for giving or personal development. This could include charity, helping family, or investing in education and skill development.

This rule is useful because it promotes discipline and ensures that income is not only spent but also saved and invested. It creates a balanced financial lifestyle.

How to start a budget for beginners?

Starting a budget as a beginner can feel overwhelming, but it becomes easy with a simple approach. The first step is to calculate your total monthly income so you know how much money you are working with.

Next, list all your expenses, including rent, food, transport, bills, and other costs. This helps you understand where your money is going.

Then, divide your expenses into needs and wants. Needs are essential for survival, while wants are optional. This step helps you prioritize spending.

After that, set a saving goal, even if it is small. Saving regularly is more important than saving large amounts occasionally.

Choose a simple budgeting method like the 50/30/20 rule or a zero-based budget, where every naira is assigned a purpose.

Finally, track your spending and review your budget monthly. Adjust it if your income or expenses change.

The key to successful budgeting is consistency. Start simple, stay disciplined, and improve gradually over time.

What are the 7 habits of highly effective college students?

Highly effective college students often share habits that help them succeed academically and financially. The first habit is clear goal setting. They define what they want to achieve each semester and work toward it consistently. The second is time management, where they plan their daily activities to balance studies, social life, and rest.

The third habit is discipline and consistency. They stick to routines, complete assignments on time, and avoid procrastination. The fourth is active learning, meaning they engage in class, ask questions, and practice regularly instead of cramming.

The fifth habit is financial responsibility. They budget their money, avoid unnecessary spending, and save when possible. The sixth is self-care, including proper sleep, healthy eating, and mental well-being, which improves productivity.

The seventh habit is continuous improvement. They seek feedback, learn from mistakes, and develop new skills beyond academics. These habits help students succeed not just in school but in life after graduation.

How to do a student budget?

Creating a student budget starts with identifying your income sources, such as allowance, part-time jobs, or support from family. This gives you a clear idea of how much money you have to manage.

Next, list your essential expenses like food, transport, books, and data. These are your priority and must be covered first. After that, include school-related costs such as materials, assignments, and projects.

Then, allocate a portion for savings, even if it is small. Saving consistently builds discipline and prepares you for emergencies.

Set a limit for wants, such as entertainment, outings, and shopping. This helps prevent overspending.

You can use a simple method like the 50/30/20 rule or adjust it to fit your situation. Finally, track your spending daily to ensure you stay within your budget.

A student budget helps you avoid running out of money before the end of the month and teaches valuable financial skills.

What are the 5 basics to any budget?

Every effective budget is built on five basic components. The first is income, which includes all the money you receive from salary, allowance, or business. Without knowing your income, budgeting is impossible.

The second is expenses, which are all the costs you incur. These can be fixed (rent, subscriptions) or variable (food, transport).

The third is prioritization, where you separate needs from wants. Essentials like food and rent must come before non-essential spending.

The fourth is savings, which should be treated as a necessary expense. This includes emergency funds and future financial goals.

The fifth is tracking and review. A budget is not complete unless you monitor your spending and adjust when necessary.

These basics ensure that your budget is practical, realistic, and effective in helping you manage your finances.

How to save money every day as a student?

Saving money daily as a student is possible with small, consistent actions. One of the easiest ways is to reduce daily spending, such as cutting down on snacks, drinks, or unnecessary purchases.

Another method is to set a daily savings target, even if it is small like ₦50–₦100. Over time, these small amounts add up significantly.

You can also cook your own meals instead of buying food frequently, which saves a lot of money in the long run. Using public or cheaper transport options also helps reduce expenses.

Avoiding impulse buying is very important. Before spending, ask yourself if the item is truly necessary.

You can also use a savings jar or mobile app to store money daily. Keeping savings separate reduces the temptation to spend it.

Finally, take advantage of student discounts and free resources whenever possible. Daily saving is not about large amounts but consistent habits that build financial discipline over time.

What are the 4 A’s of budgeting?

The 4 A’s of budgeting are simple principles that help guide effective money management. The first is Awareness, which means understanding how much you earn and how you spend your money. Without awareness, budgeting becomes guesswork.

The second is Allocation, where you assign your income to different categories such as needs, wants, and savings. This ensures every part of your money has a purpose.

The third is Adjustment, which involves modifying your budget when circumstances change. For example, if your income drops or expenses increase, your budget should adapt accordingly.

The fourth is Accountability, which means tracking your spending and holding yourself responsible for following your budget. This step ensures discipline and consistency.

Together, these four principles create a strong foundation for budgeting and help individuals maintain control over their finances.

What is the 3 6 9 rule of money?

The 3–6–9 rule of money is a simple guideline for building an emergency fund based on how many months of your expenses you can cover. It is designed to protect you from financial shocks like job loss, reduced income, or unexpected bills.

The first level is 3 months of expenses, which is considered the minimum safety net. It is suitable for people with stable income or strong family support. This amount can help you handle short-term disruptions without borrowing money.

The second level is 6 months of expenses, which provides stronger financial security. It is recommended for people with moderate income uncertainty, such as freelancers or students relying on irregular support. This gives you more time to recover from financial setbacks.

The third level is 9 months of expenses, which offers maximum protection. It is ideal for individuals with unpredictable income or high responsibilities. This level ensures you can survive longer periods without income.

The goal of this rule is to build financial confidence and reduce reliance on debt during emergencies. It also encourages disciplined saving over time.

How to budget as a 17 year old?

Budgeting at 17 is a great way to build lifelong money skills. The first step is to identify your income sources, such as allowance, gifts, or part-time work. Even small amounts can be managed effectively with the right approach.

Next, list your basic expenses, which may include transport, school supplies, data, and personal items. These should come before spending on entertainment or luxury items.

Then, divide your money into three parts: needs, wants, and savings. A simple rule like 50/30/20 works well, where you save at least 20% of your income.

It’s also important to set a savings goal, such as buying a gadget, funding education, or building an emergency fund. Having a goal keeps you motivated.

Track your spending regularly using a notebook or mobile app. This helps you avoid wasting money on unnecessary things.

Most importantly, learn to delay gratification. Not every desire needs immediate spending. Budgeting at your age is about learning control, not restriction.

What is the 40-40-20 budget rule?

The 40-40-20 budget rule is a financial strategy that divides your income into three main parts to balance spending and saving.

The first 40% is allocated to essential living expenses such as rent, food, transport, and utilities. This ensures your basic needs are covered.

The second 40% is dedicated to savings and investments. This is a more aggressive savings strategy compared to other budgeting rules. It focuses on building wealth quickly by prioritizing saving and investing a large portion of your income.

The remaining 20% is used for wants and lifestyle expenses, such as entertainment, shopping, and leisure activities.

This rule is especially useful for individuals who want to grow their wealth faster or achieve financial independence. However, it may be difficult to follow for people with low income or high living costs.

The key benefit is that it forces strong financial discipline and prioritizes long-term financial growth over short-term enjoyment.

What is the biggest expense item for teenagers?

The biggest expense item for teenagers usually falls under lifestyle and discretionary spending rather than essential needs. This includes things like food outside the home, entertainment, fashion, gadgets, and data subscriptions.

Among these, food and snacks are often the largest daily expense. Many teenagers spend money frequently on fast food, drinks, and snacks, which adds up quickly over time.

Another major expense is data and subscriptions, especially with heavy use of social media, streaming platforms, and online games.

Clothing and fashion also take a large portion of teenage spending, as many want to keep up with trends or peer expectations.

Transportation can also be a significant cost, especially for students who commute daily.

The main issue is that these expenses are often unplanned and repetitive, making them harder to control. Learning to track and limit these costs can help teenagers save more effectively.

What are 5 good financial goals?

Setting financial goals helps give direction to your money and improves discipline. One important goal is building an emergency fund, which protects you during unexpected situations like medical issues or loss of income.

The second goal is saving a fixed percentage of your income regularly. This creates consistency and helps you grow your money over time.

The third goal is reducing or eliminating debt. Paying off loans improves your financial freedom and reduces stress.

The fourth goal is investing for the future, whether through business, education, or financial assets. This helps increase your income potential over time.

The fifth goal is developing a valuable skill that can generate income. Skills like digital marketing, design, or tech can significantly improve your earning ability.

These goals are effective because they focus on both short-term stability and long-term growth, helping you build a strong financial foundation.