Managing money in Nigeria has become more challenging as the cost of living continues to increase.

Everyday expenses such as food, transportation, electricity bills, mobile data, and household needs now consume a larger portion of people’s income than before.

Because of these constant price changes, many people create monthly budgets but struggle to follow them until the end of the month.

Unexpected expenses, poor spending habits, and lack of regular tracking often make monthly budgets difficult to maintain.

Weekly budgeting offers a more practical and realistic approach. Instead of trying to control spending for an entire month at once, a weekly budget allows you to focus on shorter periods, making it easier to monitor expenses, adjust quickly, and avoid running out of money before the month ends. It also helps people become more aware of where their money goes each week.

Most importantly, budgeting is not reserved for people with high incomes. Whether you earn daily, weekly, or monthly, creating a realistic weekly budget can help you manage your money better, reduce unnecessary spending, and build healthier financial habits over time.

What a Weekly Budget Means

A weekly budget is a money management method where you plan, allocate, and track your spending every seven days instead of budgeting for an entire month at once.

It involves dividing your available income into weekly portions and assigning each portion to important categories such as food, transport, bills, savings, and personal expenses.

The goal is to make spending easier to control and reduce the chances of exhausting your money too early.

Unlike monthly budgeting, which requires planning for 30 or 31 days in one attempt, weekly budgeting breaks financial decisions into smaller and more manageable periods.

Monthly budgets can look organized on paper, but many people struggle to stay disciplined for an entire month because unexpected expenses often arise.

Weekly budgeting creates regular checkpoints that allow you to review your spending, make adjustments, and stay on track before small mistakes become major financial problems.

This budgeting style works especially well for people with irregular income, such as freelancers, business owners, traders, side hustlers, commission earners, and people whose earnings change from week to week.

Since income may not come in fixed amounts or on fixed dates, managing finances weekly allows more flexibility and quicker adjustments.

Weekly budgeting is also useful for salary earners. Even when receiving a monthly salary, dividing funds into weekly limits can reduce overspending during the first few days after payment and create better spending discipline throughout the month.

For example, if your monthly income is ₦120,000, instead of trying to manage the entire amount for 30 days at once, you can divide your spending into weekly portions.

After setting aside fixed bills and savings, the remaining money can be allocated across four weeks. This approach makes it easier to know your weekly spending limit and avoid financial pressure before the next payday.

Calculate Your Total Weekly Income

The first step in creating a realistic weekly budget is to clearly understand how much money you actually earn within a specific period.

Without knowing your true income, it becomes very easy to overestimate what you can afford and end up spending more than you should. Your weekly income should be based on actual cash received, not money you expect or hope to get.

For salary earners, this process is usually more straightforward. If you receive a fixed monthly salary, you can divide it into weekly portions to get an estimated weekly income.

However, it is important to first subtract fixed obligations such as rent savings, debt repayments, or mandatory bills before dividing the remaining amount for weekly spending. This ensures your budget reflects what is truly available for daily living.

For business owners and traders, income may fluctuate from week to week. In this case, it is better to calculate an average based on your earnings over the past few weeks or months.

This helps you set a realistic weekly target instead of relying on your best-performing weeks, which may not always be consistent.

Side hustle earners and freelancers should also calculate their income based only on confirmed payments received.

Since these earnings can vary, it is safer to base your weekly budget on conservative estimates rather than optimistic expectations. This helps prevent financial stress when income is lower than expected.

A simple method to estimate weekly income is:

Monthly income ÷ 4 = estimated weekly income

However, this formula should only be applied to money you actually receive. It is important to avoid budgeting based on expected payments, pending jobs, or uncertain income sources.

A realistic budget is built on confirmed income, not assumptions. This approach helps you stay financially stable and avoid spending money you have not yet earned.

Track Your Current Weekly Spending

Before you can create a realistic weekly budget, you need a clear picture of where your money is currently going.

Many people underestimate their spending because they do not actively track it, which leads to financial confusion and constant shortages before the end of the week.

Tracking your expenses helps you understand your real spending habits and identify areas where adjustments are needed.

Start by breaking your spending into clear categories. One of the biggest expenses for most people in Nigeria is food, which includes groceries, eating out, and small daily purchases.

Transportation is another major category, especially for those who commute daily for work, school, or business. Airtime and data costs also add up quickly due to constant communication and internet usage.

Electricity expenses, such as prepaid meter recharge or estimated billing, should also be included, as they often come unexpectedly or vary from week to week.

If you support your family financially, this should be recorded as a separate category because it is a consistent obligation for many people.

Rent contribution or savings toward housing should also be tracked, even if it is a small weekly contribution rather than a monthly payment.

Savings must be treated as a fixed part of your spending, not what is left over after expenses. Treating savings this way helps build financial discipline.

Additionally, you should account for unexpected expenses such as medical needs, repairs, emergencies, or unplanned social commitments, which often disrupt poorly planned budgets.

Advice: To track effectively, write down every expense for at least one week without changing your spending habits.

Use a notebook or mobile budgeting app to record everything immediately after spending.

This will give you a truthful reflection of your financial behavior and make it easier to build a realistic weekly budget that matches your lifestyle instead of an ideal version of it.

Separate Needs from Wants

One of the most important steps in building a realistic weekly budget is learning how to clearly separate needs from wants.

This distinction helps you prioritize essential spending and avoid wasting money on things that do not directly support your survival or financial stability.

Needs are the basic expenses required for daily living and must be covered first in any budget.

These include feeding, transportation to work or school, rent or housing contributions, utility bills such as electricity and water, and other essential responsibilities that keep life running smoothly.

Without meeting these needs, it becomes difficult to function properly or maintain a stable lifestyle.

Wants, on the other hand, are non-essential expenses that improve comfort or enjoyment but are not necessary for survival.

These include eating out frequently, impulse online shopping, excess subscriptions to streaming or digital services, and luxury purchases that are not urgently needed.

While wants are not bad, they should only be considered after needs and savings have been fully taken care of within your weekly budget.

In Nigeria, many people often confuse wants with needs, which leads to financial stress.

For example, regularly eating fast food or ordering food online may feel like a necessity due to convenience, but it is actually a want that can be reduced or controlled.

Similarly, upgrading phones frequently or subscribing to multiple entertainment services at the same time can drain income that should be reserved for more important expenses.

Even transportation choices can sometimes shift from need to want when more expensive options are chosen without financial planning.

Understanding this difference helps you make better financial decisions. When you clearly identify what is essential and what is optional, you gain better control over your money and reduce unnecessary spending.

Over time, this habit strengthens your financial discipline and makes your weekly budget more realistic, balanced, and effective in managing your income.

Set Spending Limits for Each Category

After identifying your income and separating your needs from your wants, the next important step is to assign clear spending limits to each category in your weekly budget.

This is where your financial discipline becomes practical because it determines how much you are allowed to spend in each area without affecting other important responsibilities.

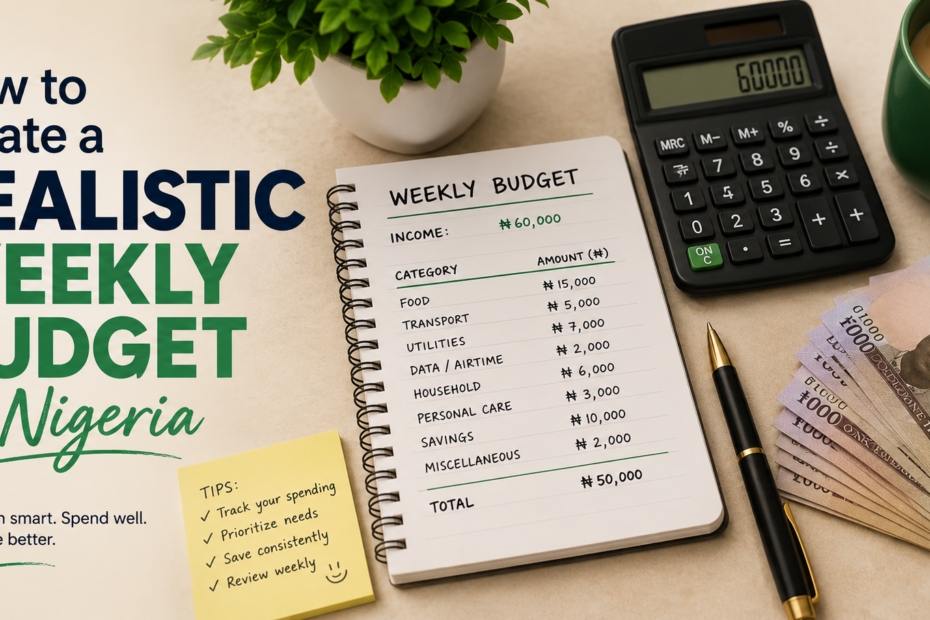

For example, if your weekly income is ₦30,000, you can divide it into realistic categories based on priority and daily needs. A simple structure could look like this:

Food — ₦10,000

Transport — ₦5,000

Savings — ₦4,000

Bills — ₦4,000

Emergency — ₦2,000

Miscellaneous — ₦5,000

This breakdown helps ensure that every naira has a purpose, reducing the chances of impulsive spending or running out of money before the week ends.

Food and transport often take a larger portion because they are daily necessities, while savings and emergency funds help you build financial stability over time.

However, it is important to understand that there is no fixed formula that works for everyone. The percentage you allocate to each category should depend on your lifestyle, income level, location, and personal responsibilities.

For example, someone living in a high-cost area may spend more on transport or rent, while someone with fewer family obligations may allocate more to savings or business investment.

The goal is not to copy a perfect template but to create a budget that reflects your real life. A realistic budget is flexible, balanced, and based on actual needs rather than unrealistic expectations.

When you set proper limits for each category and stick to them consistently, you gain better control over your money and reduce financial stress throughout the week.

Include an Emergency Buffer

An important part of a realistic weekly budget is setting aside an emergency buffer. This is a small amount of money reserved specifically for unexpected expenses that can disrupt your normal spending plan.

In a country like Nigeria, where prices and situations can change quickly, an emergency buffer helps you stay financially stable even when surprises occur.

Common examples of emergencies include sudden increases in transport fares, which often happen due to fuel price changes or road conditions.

Medical needs are another major reason to have a buffer, as health issues can arise without warning and may require immediate spending.

Fuel price fluctuations can also affect both transportation and business costs, making it important to have extra funds available.

Additionally, unexpected family expenses such as urgent support for relatives, ceremonies, or unforeseen obligations can easily affect your weekly budget if you are not prepared.

Without an emergency buffer, many people are forced to borrow money or cut into essential spending categories like food or savings, which can create financial stress and imbalance.

A buffer acts as a safety net that protects your main budget categories from being disrupted.

It is recommended to set aside about 5–10% of your weekly income as an emergency buffer. This percentage is small enough to remain manageable but large enough to make a difference when unexpected expenses occur.

For example, even if your income is modest, consistently saving this portion every week builds a reliable cushion over time.

The goal is not just to plan your money but to protect it. An emergency buffer ensures that your weekly budget remains realistic and flexible, helping you handle life’s uncertainties without losing control of your finances.

Use Simple Budgeting Methods

A realistic weekly budget is easier to maintain when you choose a simple method that fits your lifestyle.

Many people struggle with budgeting not because they lack income, but because they use complicated systems they cannot consistently follow.

Simple budgeting methods help you stay disciplined, track your money clearly, and reduce unnecessary spending.

The envelope method is one of the oldest and most effective budgeting techniques. It involves dividing your weekly income into different categories and placing the cash for each category into separate envelopes.

For example, you may have envelopes for food, transport, savings, and miscellaneous expenses. Once the money in an envelope is finished, you cannot spend more in that category until the next budgeting cycle.

This method works well because it creates physical limits and reduces the temptation to overspend. It is especially useful for people who struggle with impulse spending or find digital tracking difficult to maintain.

Cash budgeting is another simple method where you withdraw your weekly budget in cash and commit to spending only from that amount.

Unlike the envelope method, you may not necessarily separate the money physically, but you still rely on cash instead of card or online payments.

This approach helps you become more aware of your spending because cash is easier to track mentally than digital transactions.

It also reduces unnecessary spending since handing over cash feels more “real” than tapping a card or phone.

The banking app tracking method uses mobile banking or fintech apps to monitor expenses automatically.

Most Nigerian banking apps now categorize transactions, making it easier to see where your money goes each week.

This method is ideal for people who prefer digital solutions and want real-time updates on their spending. It helps you identify patterns quickly and adjust your budget without waiting until the end of the week.

The spreadsheet method involves using tools like Excel or Google Sheets to record income and expenses.

You manually enter your weekly earnings and spending, which gives you full control and detailed insight into your financial habits.

This method is great for people who like structure and want to analyze their money more deeply. It also allows you to plan future budgets based on past spending patterns.

The notebook budgeting method is a traditional but highly effective approach. It involves writing down all income and expenses in a physical notebook.

This method works well for people who prefer simplicity and do not rely heavily on digital tools.

Writing things down helps improve awareness and discipline because you are actively recording every transaction. It may be simple, but it is powerful for building consistent financial habits.

Avoid Common Weekly Budget Mistakes

Even with a well-planned weekly budget, many people still struggle financially because of simple but costly mistakes.

Avoiding these errors is just as important as creating the budget itself, because one wrong habit can disrupt your entire financial plan.

One common mistake is forgetting small expenses. Many people focus only on big costs like food, transport, or rent, while ignoring small daily spending such as snacks, tips, data top-ups, or impulse purchases.

These “small” expenses add up quickly over the week and can silently consume a large part of your income without you noticing. If they are not included in your budget, they will always cause shortages.

Another major mistake is overspending early in the week. This happens when someone receives income and spends too much in the first few days, leaving little or nothing for the remaining days.

This behavior often leads to borrowing or cutting back on essential needs later in the week. A weekly budget should be spread evenly and controlled, not consumed quickly.

Copying another person’s budget is also a serious error. Everyone has different income levels, family responsibilities, transportation costs, and lifestyle needs.

What works for one person may not work for another. A budget must reflect your personal reality, not someone else’s financial situation.

Ignoring inflation is another mistake that affects many Nigerians. Prices of food, fuel, and transportation change frequently, and failing to adjust your budget accordingly can make your estimates unrealistic.

A flexible budget should be reviewed and updated to match current economic conditions.

Finally, not reviewing your budget weekly can lead to repeated financial mistakes. A weekly review helps you understand what worked, what failed, and what needs adjustment.

Without this habit, you keep repeating the same errors and never improve your financial discipline. Regular reflection is key to building a strong and realistic budgeting habit.

How to Stay Consistent With Your Budget

Creating a weekly budget is only the first step; the real challenge is staying consistent with it.

Many people start with good intentions but abandon their budget after a few days when spending habits or unexpected situations disrupt their plan. Consistency is what turns budgeting from a temporary effort into a long-term financial habit.

One effective way to stay consistent is by doing a weekly review every Sunday.

This is a simple habit where you sit down at the end of the week to check how you spent your money, what categories you stayed within, and where you went over budget.

This reflection helps you understand your financial behavior and prepares you for the upcoming week. It also allows you to make corrections before the next cycle begins, ensuring that mistakes are not repeated.

Another important practice is adjusting your budget when prices change. In Nigeria, the cost of food, transport, and fuel can change quickly due to inflation and market conditions.

A realistic budget is not fixed forever; it should be flexible enough to reflect current economic realities. When prices increase, you may need to slightly reduce spending in other categories or adjust your allocations to maintain balance.

Tracking your progress is also essential for staying motivated. This means monitoring how well you stick to your spending limits and observing improvements over time.

You might notice that you are spending less on unnecessary items or saving more consistently. These small wins build confidence and encourage better financial discipline.

Finally, rewarding discipline without overspending can help you stay committed. When you successfully stick to your budget for a week or month, you can reward yourself with a small, controlled treat.

This could be something simple and affordable that does not disrupt your financial plan. The goal is to encourage positive behavior without falling back into unnecessary spending habits.

Consistency is what transforms budgeting from theory into real financial control. When you review, adjust, track, and reward yourself wisely, your weekly budget becomes a sustainable system that supports your financial goals.

Sample Real-Life Scenario

To make weekly budgeting more practical, it helps to see how it works in real life. Many people understand budgeting better when they can relate it to a real situation instead of just theory.

Below are two simple scenarios showing how different people can manage their weekly income effectively in Nigeria.

A common example is how a student survives ₦15,000 weekly. A student in a university or polytechnic often has limited income from parents, allowances, or small side jobs.

With ₦15,000 for a week, the first priority is feeding, which may take around ₦6,000 to ₦7,000 depending on location and lifestyle.

Transport may take about ₦2,000 to ₦3,000 if the student moves between lectures or off-campus activities. Airtime and data could take around ₦1,000, especially for academic research and communication.

A small portion, maybe ₦1,000 to ₦2,000, should be set aside for savings or emergency needs. The remaining amount can be used for miscellaneous expenses such as printing, small personal items, or unexpected school costs.

The key here is discipline—avoiding unnecessary spending like frequent eating out or impulse purchases helps the student survive the week without financial stress.

Another example is how a worker manages ₦50,000 weekly expenses. A salary earner or junior worker with this amount must balance multiple responsibilities.

Food might take around ₦15,000, while transport could require ₦10,000 depending on daily commuting distance.

Savings should be a priority, so allocating about ₦7,000 to ₦10,000 helps build financial stability over time. Utility bills or family support may take another ₦8,000 to ₦10,000.

An emergency buffer and miscellaneous expenses can take the remaining balance. This structure ensures that essential needs are covered while still allowing room for savings and unexpected costs.

These scenarios show that budgeting is not about how much you earn, but how well you manage what you have.

Whether the income is small or large, a realistic weekly budget helps you stay in control, avoid debt, and build better financial habits over time.

Conclusion

A realistic weekly budget is not about copying strict financial rules or trying to live like someone else; it is about building a system that fits your actual income and lifestyle.

When your budget reflects what you truly earn and spend, it becomes easier to follow and more effective in helping you stay financially stable. The goal is not perfection, but consistency and honesty with your money.

Small weekly decisions play a powerful role in shaping your long-term financial future.

Every time you choose to save instead of overspend, track your expenses instead of guessing, or stick to your limits instead of borrowing, you are building financial discipline. Over time, these small actions accumulate and create real stability, even if your income is modest.

It is also important to understand that progress matters more than perfection. No one gets budgeting completely right from the beginning.

Some weeks may go well, while others may be difficult due to unexpected expenses or mistakes. What matters is your ability to learn, adjust, and continue improving your financial habits instead of giving up.

In today’s Nigeria, where the cost of living continues to rise and income can be unpredictable, budgeting is no longer just a financial skill—it is becoming a survival skill.

Those who learn how to manage their money weekly are better prepared to handle economic challenges, reduce stress, and build a more secure future.

Ultimately, a realistic weekly budget gives you control, clarity, and confidence over your finances. It helps you live within your means while still planning for growth, stability, and better opportunities ahead.

Frequently Asked Questions

What is the 50/30/20 rule for weekly pay?

The 50/30/20 rule is a simple and widely used budgeting framework that helps individuals manage their income in a balanced and structured way.

Although it is often explained using monthly income, it can also be applied effectively to weekly pay, especially for people who earn salaries or wages on a weekly basis.

The rule divides your income into three main categories: 50% for needs, 30% for wants, and 20% for savings or debt repayment.

The first category, which is 50% for needs, covers essential expenses that you cannot avoid in your daily life. These include food, transportation, rent or accommodation, utilities, basic clothing, and other survival-related costs.

For someone earning weekly income, this means half of the money should immediately go toward keeping life stable and functional.

If this portion is too high, it usually indicates that lifestyle costs are too expensive compared to income.

The second category, 30% for wants, represents lifestyle choices and non-essential spending. This includes entertainment, data subscriptions, eating out, fashion, streaming services, and social activities.

These are things that improve quality of life but are not necessary for survival. The idea is not to eliminate enjoyment but to control it so that it does not interfere with financial stability.

The final category, 20% for savings or debt repayment, is what builds financial security. This portion can go into savings, emergency funds, investments, or paying off loans.

Over time, this part becomes the foundation for financial growth and protection against unexpected expenses like medical bills or job loss.

When applied to weekly income, the rule encourages discipline by breaking spending into smaller time frames. Instead of waiting for month-end to manage money, you plan every week.

This makes budgeting more realistic and easier to follow, especially in environments where income and expenses fluctuate frequently.

Overall, the 50/30/20 rule is powerful because it is simple, flexible, and encourages both responsible spending and long-term financial growth.

What is the 70-10-10-10 budget rule?

The 70-10-10-10 budget rule is a financial planning method that divides income into four structured categories to help individuals manage money in a more disciplined and intentional way.

It is particularly useful for people who want a simple system that still allows room for living expenses, savings, investment, and giving or emergency planning.

Unlike more traditional budgeting models, this approach adds more flexibility by spreading income across four clear purposes.

The largest portion, which is 70%, is allocated to living expenses. This covers all essential and day-to-day costs such as rent, food, transportation, utility bills, school fees, and basic personal needs.

The idea is that most of your income will naturally go into survival and lifestyle maintenance. However, keeping this at 70% also encourages discipline, because it prevents lifestyle inflation from consuming all earnings.

The next portion, 10%, is dedicated to savings. This is money set aside for future use, whether for planned goals like buying a phone, building an emergency cushion, or handling unexpected situations.

Even though 10% may seem small, consistency over time builds financial stability and reduces dependence on loans during emergencies.

Another 10% is allocated to investment or personal development. This could include starting a small business, investing in stocks or mutual funds, learning a new skill, or paying for courses that improve earning potential. This part of the budget focuses on growth and future income improvement.

The final 10% is often used for giving, charity, or flexibility spending. Some people use it for donations, supporting family, or covering unexpected social expenses.

It also provides emotional balance, because it allows you to spend without guilt while still staying within structure.

Overall, the 70-10-10-10 rule works well for people who want a practical budgeting system that reflects real-life needs, especially in environments where income is limited or expenses are unpredictable.

It ensures survival, encourages saving, promotes growth, and still allows generosity or flexibility.

How to make a monthly budget in Nigeria?

Creating a monthly budget in Nigeria requires a realistic understanding of income, expenses, and the economic environment, where prices of goods and services can change frequently.

The first step is to calculate your total monthly income. This includes salary, business profits, side hustles, and any other consistent earnings.

It is important to use a conservative estimate so that you do not overestimate your financial capacity.

The next step is to list all essential expenses. These typically include rent, foodstuff, transportation, electricity (PHCN or generator fuel), internet data, school fees if applicable, and basic family support.

In Nigeria, transportation and food often take a large portion of income due to inflation and fluctuating prices, so it is important to research current costs rather than guess.

After listing essentials, the next step is to identify non-essential or flexible expenses. These may include entertainment, eating out, fashion items, subscriptions, and impulse purchases.

These are the areas where adjustments can be made if income is not enough. A good budget always separates needs from wants clearly.

The fourth step is to allocate savings. Even if income is small, setting aside a fixed percentage or amount is important.

This could be for emergencies, future investments, or long-term goals. In Nigeria, where unexpected expenses like medical bills or urgent family needs are common, having savings is crucial.

The fifth step is to adjust your budget based on reality. If expenses are higher than income, you must reduce spending or increase income through side hustles or small businesses.

A budget is not fixed; it should reflect real-life conditions and be updated monthly as prices change.

Finally, track your spending throughout the month. Many people in Nigeria struggle with budgeting because they create plans but do not monitor execution. Using notes, apps, or simple records helps ensure discipline.

A well-made monthly budget gives financial control, reduces stress, and helps you prepare better for rising living costs in Nigeria.

What are the 7 steps for preparing a budget?

Preparing a budget involves a structured process that helps individuals or households take control of their finances and make intentional decisions about money.

The first step is to identify your income sources. This includes salary, business income, freelance work, side hustles, or any other form of regular earnings.

Knowing your total income is important because it sets the foundation for everything else in the budget.

The second step is to list all fixed expenses. These are expenses that remain relatively constant every month, such as rent, school fees, subscriptions, loan repayments, and transportation costs. Fixed expenses are important because they are unavoidable and must be prioritized.

The third step is to estimate variable expenses. These include food, utilities, fuel, clothing, and other costs that can change from month to month.

In places like Nigeria, variable expenses can fluctuate significantly due to inflation, so careful estimation is important.

The fourth step is to categorize your spending into needs, wants, and savings. This helps you understand where your money is going and ensures that essential needs are prioritized over unnecessary spending.

The fifth step is to set financial goals. These could include saving for emergencies, investing, paying off debt, or planning for a major purchase. Clear goals give your budget direction and motivation.

The sixth step is to allocate your income according to priorities. This means assigning specific amounts to each category based on importance and affordability. It ensures that money is not spent randomly.

The final step is to monitor and adjust your budget regularly. A budget is not a one-time activity; it must be reviewed weekly or monthly to reflect changes in income, prices, or financial goals.

When these seven steps are followed consistently, budgeting becomes a powerful tool for financial stability and long-term success.

What are 20 examples of expenses?

Expenses refer to the various costs individuals or households spend money on in daily life. Understanding these examples helps in creating a realistic budget and tracking where money goes.

One common expense is rent or housing, which includes monthly payments for accommodation. Another is food, which covers groceries, meals, and daily nutrition costs.

Transportation is also a major expense, including fuel, public transport fares, ride-hailing services, and vehicle maintenance.

Electricity bills are another example, especially in areas where power supply requires alternative energy sources like generators or solar systems.

Water bills, internet data subscriptions, and phone airtime are also regular expenses for communication and daily living.

School fees or educational costs are important expenses for families with children or individuals in training programs.

Healthcare expenses include hospital visits, medication, and medical insurance where available. Clothing and personal care items such as toiletries, haircuts, and grooming products also fall under regular spending.

Entertainment expenses include movies, streaming subscriptions, gaming, and social outings. Debt repayment is another important category, covering loans, credit payments, or borrowed money.

House maintenance costs, such as repairs or cleaning services, are also included. Furniture or household items like kitchen supplies or appliances are occasional but necessary expenses.

Other examples include insurance payments, charity or donations, mobile phone upgrades, and unexpected emergency costs.

Business-related expenses like inventory, equipment, or marketing are also common for entrepreneurs.

Finally, miscellaneous expenses cover small, unplanned spending that does not fit into a specific category.

Together, these 20 examples show how diverse daily financial obligations can be. Identifying them clearly helps individuals understand spending habits and build a more effective budget.

Can ChatGPT make me a budget?

Yes, ChatGPT can help you create a personalized budget based on your income, lifestyle, and financial goals.

The process is usually simple: you provide details such as your monthly or weekly income, your fixed expenses like rent, transport, feeding, and utilities, as well as your financial goals such as saving, investing, or paying off debt.

Based on this information, a structured and realistic budget can be created to match your situation.

What makes ChatGPT useful for budgeting is its ability to break down your income into clear spending categories and suggest improvements.

For example, if your expenses are too high compared to your income, it can recommend adjustments such as reducing non-essential spending or increasing savings contributions.

It can also help you apply budgeting systems like the 50/30/20 rule or 70-10-10-10 rule depending on what fits your lifestyle.

In addition, ChatGPT can help you plan for real-life situations, especially in environments like Nigeria where prices fluctuate.

It can assist in building flexible budgets that can be adjusted when food prices, transport fares, or bills change. It can also help you design weekly or monthly budget templates, track spending habits, and set realistic savings goals.

However, it is important to understand that ChatGPT does not track your money automatically or connect to your bank account.

Instead, it works as a planning and advisory tool. You still need to apply the budget manually and monitor your spending yourself or with a budgeting app.

Overall, ChatGPT can act like a personal financial assistant by helping you organize your income, control spending, and build better financial discipline. If you provide your income details, I can even create a full custom budget plan for you.

What are the 7 types of budgeting?

There are several budgeting methods used in personal finance and business planning, and each one serves a different purpose depending on financial goals and discipline level.

One common type is incremental budgeting, where the previous budget is adjusted slightly based on changes in income or expenses. It is simple but may not always encourage major financial improvements.

Another type is zero-based budgeting, where every income is assigned a specific purpose so that income minus expenses equals zero.

This method forces full accountability and ensures that every naira or dollar is planned for, leaving no unassigned money.

The envelope budgeting system is also widely used, especially for personal finance.

It involves dividing money into categories and physically or digitally allocating cash into envelopes for spending control. Once an envelope is empty, spending in that category stops.

The rolling budget is another type, where the budget is continuously updated by adding a new period as the current one ends. This helps maintain an ongoing financial plan that always looks ahead.

The flexible budget adjusts based on actual income or business performance. It is commonly used in businesses where income is not fixed, allowing expenses to rise or fall depending on revenue.

The activity-based budget focuses on the cost of activities required to run a business or household. Instead of just estimating expenses, it links spending directly to tasks or operations.

Finally, the value proposition budgeting method prioritizes spending based on value and impact rather than fixed categories. It ensures money is spent on what brings the most benefit or return.

Together, these seven budgeting types provide different ways to manage money depending on discipline, income stability, and financial goals.

What is the budgeting app in Nigeria?

There are several budgeting apps used in Nigeria that help individuals track expenses, manage income, and improve financial discipline.

One of the most popular is Kuda Bank, a digital bank that offers built-in budgeting and spending tracking features.

It allows users to monitor transactions in real time and categorize spending automatically, making it easier to control money flow.

Another widely used app is PiggyVest, which focuses strongly on savings and disciplined money management.

It allows users to lock funds, save automatically, and set financial goals. Many Nigerians use it to build emergency funds or save for long-term projects.

ALAT by Wema is also a well-known budgeting and digital banking platform. It provides savings plans, bill payments, and budgeting tools that help users manage money efficiently within one app.

Carbon is another financial app that offers spending insights, loans, and money management tools. It helps users track expenses while also giving access to credit when needed.

For simple expense tracking, apps like Money Manager and Spendee are also used by Nigerians who prefer manual budgeting with clear visual reports of income and spending patterns.

These apps are important because they help users in Nigeria deal with fluctuating income, rising living costs, and the challenge of maintaining financial discipline. They also reduce the need for manual record keeping by automatically categorizing transactions.

Overall, the best budgeting app depends on your goal—whether it is saving, tracking expenses, or managing digital banking—but Kuda and PiggyVest remain among the most widely trusted in Nigeria.

What are the top 3 biggest expenses?

The top three biggest expenses for most individuals and households are usually housing, food, and transportation.

These three categories consistently take up the largest portion of income regardless of location, but they are especially significant in countries like Nigeria where living costs can vary widely.

Housing is typically the largest expense. This includes rent, mortgage payments, or accommodation costs.

In urban areas like Lagos, rent can consume a major percentage of monthly income, making it the most financially demanding responsibility for many people.

Food is the second major expense. This includes groceries, daily meals, cooking supplies, and occasional dining out.

Due to inflation and fluctuating food prices, food expenses often increase unpredictably, making it a major factor in budgeting.

Transportation is the third biggest expense. This includes daily commuting costs such as buses, taxis, fuel for vehicles, and maintenance.

In cities with heavy traffic like Lagos, transportation costs can be high because of frequent movement and rising fuel prices.

These three expenses are considered essential because they directly affect survival and daily functioning. After covering them, most people allocate what remains to utilities, savings, education, healthcare, and entertainment.

Understanding these major expense categories is important because they help individuals identify where most of their income goes.

Once these are controlled effectively, it becomes easier to save money and improve financial stability.

What are the 3 P’s of budgeting?

The 3 P’s of budgeting generally refer to Plan, Prioritize, and Practice, which are three key principles that guide effective money management.

These principles help individuals create a simple but powerful financial structure that improves discipline and long-term stability.

The first P, Plan, means setting clear financial goals and designing a budget before spending money.

Planning involves estimating income, listing expenses, and deciding how money will be allocated. Without planning, money is often spent impulsively, leading to financial stress and lack of control.

The second P, Prioritize, focuses on identifying what is most important. This means distinguishing between needs and wants and ensuring that essential expenses like food, rent, and transportation come first.

It also includes prioritizing savings and debt repayment before unnecessary spending. Prioritization helps prevent wasteful spending and ensures financial goals are achieved.

The third P, Practice, refers to consistently following the budget. Many people create budgets but fail to stick to them.

Practicing budgeting means tracking expenses daily or weekly, reviewing financial progress, and adjusting when necessary. It also involves building discipline over time so that budgeting becomes a habit rather than a task.

Together, the 3 P’s create a strong foundation for financial management. Planning gives direction, prioritizing ensures focus, and practicing builds consistency.

When applied properly, they help individuals avoid debt, build savings, and achieve financial stability over time.