In Nigeria today, earning a monthly salary of ₦100,000 may sound like a decent income, but in reality, it often does not stretch as far as many people expect. With the rising cost of living, this amount can quickly feel insufficient once basic expenses start coming in.

Every month, a large portion of income goes into essential needs like rent or accommodation, food, transport, and data. These are unavoidable expenses that continue to increase due to inflation and unstable market prices. After covering just these basics, there is often very little left.

Because of this, many people still struggle financially despite earning ₦100k. Instead of having savings or financial stability, they find themselves living from salary to salary, and sometimes even borrowing before the next payday. The problem is not always the income itself, but how it is managed.

This is where budgeting becomes very important. Without a clear plan, money gets spent quickly and without direction. But with proper budgeting, even a ₦100,000 salary can be organized in a way that covers needs, allows some comfort, and still makes room for savings.

In this guide, you will learn how to budget a ₦100,000 monthly salary in Nigeria effectively, so you can take control of your finances instead of letting your income control you.

Why ₦100,000 Can Still Feel Insufficient

Even though ₦100,000 is a regular monthly salary for many Nigerians, it often does not feel like enough due to several real-life financial pressures.

One major reason is inflation and rising prices. The cost of basic goods and services such as food, transport, rent, and utilities keeps increasing. What ₦100,000 could comfortably cover in the past may now only handle a portion of monthly needs. This constant price increase reduces purchasing power and makes budgeting more difficult.

Another factor is family responsibilities or personal expenses. Many salary earners are not only responsible for themselves but also support parents, siblings, or other dependents. When financial responsibilities are shared across multiple people, the salary quickly gets divided and stretched thin.

There is also lifestyle pressure and peer influence. Social expectations can lead people to spend on outings, fashion, gadgets, and entertainment even when their income is limited. Trying to “keep up” with others often leads to overspending and reduces the ability to save or invest.

In simple terms, ₦100,000 may look enough on paper, but real-life demands often make it feel insufficient. This is why proper budgeting is necessary—to help prioritize spending, manage pressure, and make the income work more effectively.

Step 1: Break Down Your Monthly Income

The first step in budgeting a ₦100,000 salary is to clearly understand how much money you actually receive after all deductions. Many people make the mistake of budgeting based on their gross salary instead of what is truly available to spend.

Start by confirming your net salary after deductions. These deductions may include taxes, pension contributions, or other workplace-related charges. What remains after these deductions is your real take-home pay, and this is the amount you should use for your budget.

Once you know your net income, you should identify the exact amount available for budgeting. This means treating your take-home pay as your full financial resource for the month. Every spending decision, from rent to feeding and transport, should be based on this figure.

Understanding your true income helps you avoid overspending and unrealistic planning. It also gives you a clear foundation for dividing your money properly across needs, wants, and savings.

In simple terms, this step ensures you are working with accurate numbers. When you know exactly how much you earn each month, it becomes easier to create a realistic and effective budget that fits your financial situation.

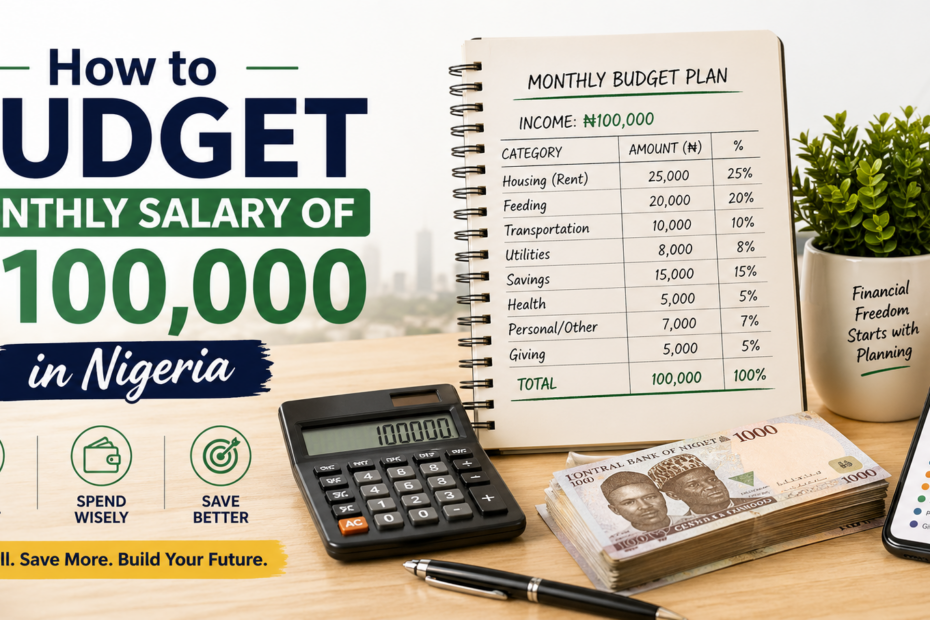

Step 2: Follow a Simple Budget Structure

After identifying your real monthly income, the next step is to organize it using a simple and realistic budget structure. This helps you distribute your ₦100,000 salary in a way that covers essentials, allows some comfort, and still supports financial growth.

A common and practical approach is:

Needs (50–60%)

This portion goes to your essential expenses such as rent or accommodation, food, transport, data, and basic utilities. In Nigeria’s current economy, this category often takes the largest share because these costs are unavoidable and constantly rising.

Wants (20–30%)

This covers lifestyle spending such as eating out, entertainment, shopping, subscriptions, and social activities. While these are not essential for survival, they are part of daily life. However, they must be controlled to avoid overspending.

Savings/Debt (10–20%)

This portion is for building savings, emergency funds, or repaying any existing debt. Even small savings matter because they provide financial security when unexpected expenses arise.

It is important to adjust for Nigerian realities. For example, if your rent or transport is high, you may need to slightly reduce your wants or savings category. The goal is not perfection, but a balance that fits your real-life situation.

In simple terms, this structure helps you control your salary instead of letting your salary control you. It gives every naira a purpose and creates financial stability over time.

Step 3: Allocate Money for Essential Needs

After setting your budget structure, the next step is to assign specific amounts to your most important expenses. These are your essential needs, and they must be prioritized because they directly affect your daily living.

Start with rent or accommodation. This is usually one of the biggest expenses in Nigeria, especially in cities. Whether you pay monthly rent or contribute to shared housing, it should be planned first so it does not disrupt your finances.

Next is food and groceries. This includes daily meals, market shopping, and basic household food items. Because food is a constant need, it is important to budget carefully and avoid unnecessary eating out that can increase costs.

Then consider transport. This covers movement to work, business activities, or daily errands. Transport costs can vary depending on location, so it is important to estimate it realistically and include it in your monthly plan.

You should also allocate money for utilities and data. This includes electricity bills, water (if applicable), airtime, and internet subscriptions. In today’s digital world, data is especially important for communication and productivity, so it must not be ignored.

In simple terms, this step ensures your basic survival needs are fully covered before spending on anything else. Once these essentials are properly allocated, you can manage the remaining income more confidently and avoid financial pressure during the month.

Step 4: Control Lifestyle Spending

After covering your essential needs, the next step is to manage how you spend on lifestyle activities. This category is important because it is where many people unknowingly lose a large part of their income.

Start with eating out. While it is convenient, frequent buying of food from restaurants or fast-food vendors is usually more expensive than cooking at home. If not controlled, it can quickly reduce the amount available for savings and other needs.

Next is shopping and entertainment. This includes buying clothes, gadgets, subscriptions, and spending on movies, streaming services, or leisure activities. These expenses are not bad on their own, but they should be planned and limited so they do not affect your financial stability.

You should also manage social expenses. This includes outings with friends, events, parties, and other social gatherings. Peer pressure can make these expenses grow quickly, especially when trying to “keep up” with others. Without control, social spending can quietly drain your monthly salary.

In simple terms, controlling lifestyle spending means making intentional choices about how you enjoy your money. It allows you to balance enjoyment with responsibility, ensuring that your salary is not consumed by non-essential expenses.

Step 5: Set Monthly Savings Goal

After managing your expenses, the next important step is to intentionally set aside money for savings. Even with a ₦100,000 salary, saving is possible if you treat it as a fixed part of your financial plan rather than something optional.

Start by building an emergency fund. This is money reserved for unexpected situations such as medical issues, urgent repairs, or sudden financial needs. Having this fund prevents you from going into debt when emergencies arise.

You should also focus on small, consistent savings. You don’t need to start big—what matters is regularity. Even setting aside a small percentage of your salary every month helps you build financial discipline and grow your savings over time.

To make saving easier, you can use financial apps like PiggyVest or Kuda. These apps allow you to automate savings, lock funds, and track progress, which reduces the temptation to spend money meant for saving.

In simple terms, setting a savings goal ensures that you are preparing for the future while managing your present needs. It turns saving into a habit, not a struggle.

Step 6: Avoid Debt and Impulse Spending

One of the fastest ways a ₦100,000 salary gets exhausted is through unnecessary debt and impulsive financial decisions. If you want your budget to work, you must actively control these habits.

Start by avoiding credit traps. This includes quick loans, “buy now pay later” offers, and borrowing for non-essential needs. While they may seem helpful in the moment, they often come with high interest or hidden pressure that reduces your future income and increases financial stress.

Next, control unplanned purchases. These are expenses you did not budget for but decide to make on the spot, such as random shopping, frequent online orders, or unnecessary upgrades. These small decisions can silently disrupt your entire monthly plan.

You should also be careful of lifestyle inflation. This happens when your spending increases just because your income improves or because you want to match others. Instead of upgrading your lifestyle immediately, it is better to maintain discipline and strengthen your savings first.

In simple terms, avoiding debt and impulse spending helps you protect your salary. It ensures that your money is used for planned needs, savings, and real priorities instead of unnecessary financial pressure.

Step 7: Track Your Budget Weekly

Creating a budget is only effective when you actively monitor how it is working. Tracking your budget weekly helps you stay aware of your spending habits and ensures you are not going off course without realizing it.

Start by monitoring your spending regularly. This means checking how much you have spent in each category—needs, wants, and savings. You can use a notebook, spreadsheet, or mobile budgeting apps to record your daily or weekly expenses. The goal is to stay aware of where your money is going at all times.

Next, be willing to adjust where necessary. A budget is not fixed forever; it should reflect your real-life situation. If you notice that transport or food costs are higher than expected, you can make small changes in other categories to balance things out.

Tracking also helps you prevent overspending. When you review your budget frequently, it becomes easier to identify when you are close to your limits and stop unnecessary spending before it gets out of control.

In simple terms, weekly tracking keeps your budget alive and effective. It helps you stay disciplined, make better decisions, and ensure your ₦100,000 salary lasts throughout the month.

Common Mistakes to Avoid

Even with a well-planned ₦100,000 budget, many people still struggle financially because of avoidable mistakes. Understanding these errors can help you manage your salary more effectively and avoid unnecessary stress.

One major mistake is having no savings plan. Some people focus only on spending and forget to set aside money for savings or emergencies. Without a savings habit, it becomes difficult to handle unexpected expenses, and this often leads to borrowing or financial instability.

Another common issue is overspending early in the month. This happens when most of the salary is spent within the first one or two weeks after payday. As a result, the remaining weeks become financially stressful, forcing people to struggle or rely on credit before the next salary arrives.

You should also avoid ignoring small expenses. Many people focus only on big bills like rent and food, while forgetting daily small spending such as airtime, snacks, transport changes, and impulse purchases. Over time, these small costs add up and significantly affect your budget.

In simple terms, these mistakes reduce financial control and make it harder to manage your salary effectively. Avoiding them helps you stay disciplined, maintain balance, and make better use of your ₦100,000 income throughout the month.

Conclusion

A ₦100,000 monthly salary may not seem like much in today’s economy, but with the right structure and discipline, it can still be enough to meet your essential needs and maintain financial stability. The difference is not always in how much you earn, but in how well you manage it.

Budgeting gives you true financial control. Instead of wondering where your money went at the end of the month, you begin to assign purpose to every naira you earn. This helps you reduce waste, avoid debt, and gradually build savings even on a modest income.

The key is consistency. When you follow a clear budget plan—covering needs, controlling wants, saving regularly, and tracking your spending—you create a system that supports your financial growth over time.

Now it’s your turn to take action. Don’t just read and move on. Your challenge is simple: create your ₦100,000 budget today and start managing your money with intention, not guesswork.

Frequently Asked Questtions

How much do you need to make a month to make 100k?

How much you need to make monthly to “make 100k” depends on what you mean by 100k—whether it is savings, profit, or disposable income after expenses. There is no single fixed answer because it is tied to your spending pattern and financial goals.

If your goal is to save ₦100,000 every month, then your income must be high enough to cover all your living expenses first. For example, if your monthly expenses (rent, food, transport, utilities, and others) are ₦150,000, then you would need at least ₦250,000 monthly income to comfortably save ₦100,000. This is because income = expenses + savings.

However, if you are asking how much you need to earn to have ₦100,000 left after expenses, then it depends on your lifestyle. A person with very low expenses might need only ₦150,000–₦180,000 monthly income to retain ₦100,000. On the other hand, someone with higher rent or responsibilities may need ₦300,000 or more.

In business terms, if your target is ₦100,000 profit, then you must also include operational costs. For example, if your business expenses are ₦200,000, you may need ₦300,000 revenue to hit ₦100,000 profit.

In summary, the amount you need to make depends on your financial structure. The lower your expenses, the easier it is to reach 100k. The key strategy is not just increasing income, but also controlling spending so that your target becomes realistic and achievable.

How to budget salary monthly in Nigeria?

Budgeting salary monthly in Nigeria requires a structured approach due to rising living costs and fluctuating expenses. The first step is to determine your total monthly income, whether it is salary, side income, or allowances. This gives you a clear starting point for planning.

Next, list your fixed expenses, such as rent, transport, electricity, internet, and school fees if applicable. These are non-negotiable costs that must be paid first. In Nigeria, rent alone can take a large portion of income, so it should be carefully planned.

After that, allocate money for food and daily needs, which are essential for survival. Then set aside a portion for savings and emergency funds, even if it is small. Consistency is more important than amount.

A useful method is the zero-based budget system, where every naira is assigned a job. This prevents wasteful spending and helps you control your finances better.

Also, include a category for transport and unforeseen expenses, since costs in Nigeria can change unexpectedly due to fuel price fluctuations or emergencies.

Finally, track your spending throughout the month using a notebook or mobile app. Adjust your budget if necessary, especially when prices increase or income changes. The goal is discipline and awareness, not perfection. Over time, this helps you achieve financial stability even on a modest salary.

What is the 70/20/10 rule budget?

The 70/20/10 rule budget is a simple money management system that divides your income into three main categories to promote financial balance. It is widely used because it is easy to understand and apply.

The first part, 70%, is allocated to living expenses. This includes rent, food, transport, utilities, and other daily needs. In a country like Nigeria where living costs can vary, this portion ensures you can comfortably cover your essential expenses.

The second part, 20%, is dedicated to savings and investments. This includes emergency funds, business investments, or long-term savings goals. This portion is very important because it helps you build financial security over time and prepares you for unexpected situations.

The final part, 10%, is used for debt repayment, charity, or personal development. This could mean paying off loans, supporting family, giving to charity, or investing in learning new skills that improve your earning ability.

The strength of this rule is its simplicity. It does not require complex calculations or financial expertise. Instead, it provides a clear structure that helps individuals avoid overspending and prioritize savings.

Overall, the 70/20/10 rule encourages discipline by ensuring that income is not only used for survival but also for future growth and financial responsibility.

Which business brings money faster in Nigeria?

Businesses that bring money faster in Nigeria are usually those with low startup costs, high demand, and quick cash turnover. One of the fastest is food business, such as selling cooked meals, snacks, or fast food. People eat daily, so demand is constant, and profit can come within days.

Another fast-income business is POS (Point of Sale) services. This is very popular in Nigeria because many people rely on agents for cash withdrawals and transfers. With proper location, daily income can start almost immediately.

Mini importation and online reselling is also profitable. Buying cheap goods from platforms and reselling locally can generate quick returns if marketing is effective.

Freelancing skills like graphic design, writing, or social media management can also bring fast money once you get clients.

Additionally, transport services like okada, keke, or ride-hailing can generate daily income, depending on location and demand.

However, fast money depends on execution, location, and consistency. No business is guaranteed; success requires effort, customer service, and proper planning. The fastest businesses are usually service-based and solve daily problems people already have.

What skills do I need to earn 100K?

To earn ₦100,000 monthly consistently, you need practical, in-demand skills that can generate value in the Nigerian market. One of the most important skills is digital marketing, which includes social media management, advertising, and content creation. Businesses are always looking for people to promote their products online.

Another valuable skill is graphic design. With tools like Canva or Photoshop, you can create logos, flyers, and branding materials for businesses. Many small businesses in Nigeria need this service.

Copywriting and content writing is also highly profitable. Businesses need words for ads, blogs, and websites, and skilled writers can earn steadily.

Tech skills like web development, app development, or UI/UX design can easily generate more than ₦100K monthly once you gain experience.

In addition, video editing and content creation for platforms like TikTok and YouTube are in high demand as online content continues to grow.

Lastly, sales and negotiation skills are essential in almost every business. Even with simple products, good selling ability can increase your income significantly.

To reach ₦100K monthly, the key is not just learning one skill but also practicing it, building experience, and offering value consistently in the marketplace.

How quickly can I turn 100K into 1 million?

Turning ₦100,000 into ₦1,000,000 depends on the strategy you use, your risk level, and consistency. In theory, you are looking for a 10× return, which is not easy to achieve quickly without high risk or strong business skills.

In low-risk savings accounts, it could take many years because interest rates are usually low in Nigeria. In moderate investments like mutual funds or small businesses, it could take 2–5 years depending on profit reinvestment and discipline.

However, in high-risk opportunities such as trading, crypto, or aggressive business scaling, it might happen within months—but it is also possible to lose money quickly if not managed well.

A more realistic approach is using business reinvestment strategy. For example, starting a small business with ₦100,000, making profit monthly, and reinvesting those profits. If you consistently grow at 20–30% monthly (which is still difficult but possible in some businesses), you could reach ₦1 million within 1–2 years.

The key factor is not just speed but sustainability. Fast gains without stability often lead to losses. The safest path is combining skill-based income + reinvestment + savings discipline to gradually grow your money.

What is considered a good salary in Nigeria?

A “good salary” in Nigeria depends on lifestyle, location, and personal responsibilities, but generally it is measured by how comfortably it covers basic needs and savings.

For many individuals, a salary between ₦150,000 to ₦300,000 monthly is considered decent, especially in smaller cities. It can cover rent, food, transport, and some savings if managed well.

In major cities like Lagos or Abuja, where the cost of living is higher, a good salary is often considered ₦300,000 to ₦700,000 monthly, especially for individuals supporting families or paying rent in urban areas.

A salary above ₦1,000,000 monthly is generally considered high income in Nigeria and allows for comfortable living, investments, and financial freedom.

However, what truly makes a salary “good” is not just the amount, but financial management skills. Someone earning ₦200,000 but managing money well may live better than someone earning ₦500,000 without discipline.

So, a good salary is one that allows you to meet needs, save consistently, handle emergencies, and still enjoy life without constant financial stress.

What are 7 ways to save money?

There are several practical ways to save money effectively, especially in a challenging economy like Nigeria. The first method is paying yourself first, which means setting aside savings immediately after receiving income before spending anything.

The second is tracking expenses, so you know exactly where your money goes each month. This helps you identify wasteful spending.

Third is creating a budget, such as the 50/30/20 rule or zero-based budgeting, to control how money is allocated.

Fourth is reducing unnecessary spending, such as impulse buying, frequent eating out, or unused subscriptions.

Fifth is automating savings, where a fixed amount is transferred into a savings account immediately after salary is received.

Sixth is buying in bulk or planning purchases, which helps reduce long-term costs on food and household items.

Seventh is setting financial goals, such as saving for rent, business, or emergency funds. Clear goals make saving more intentional and consistent.

Together, these methods build strong financial discipline and help you grow savings over time, even with a limited income.

How should I divide my monthly salary?

Dividing your monthly salary properly helps you maintain financial balance and avoid running out of money before the end of the month. One of the most common methods is the 50/30/20 rule.

In this system, 50% of your salary goes to essential needs such as rent, food, transport, and utilities. These are non-negotiable expenses required for daily living.

About 30% is allocated to wants, which include entertainment, shopping, dining out, and lifestyle expenses. This portion allows you to enjoy life while still staying within limits.

The remaining 20% is for savings and debt repayment, which helps you build financial security and reduce financial stress over time.

If your income is unstable or low, you may need to adjust this structure. For example, you might prioritize 60% needs, 20% savings, and 20% wants, or use a zero-based budget where every naira is assigned a purpose.

The most important principle is intentional allocation. Every part of your salary should have a job so that you are not left wondering where your money went.

Is 1,000,000 naira a lot in Nigeria?

₦1,000,000 in Nigeria is considered a significant amount of money, but its value depends on how it is used and the lifestyle of the person holding it.

For many individuals, ₦1 million can cover several months of living expenses. For example, it can pay rent, food, transport, and other basic needs for a few months depending on location and spending habits. In smaller towns, it stretches even further than in big cities like Lagos or Abuja.

It is also enough to start or invest in a small business, such as food sales, POS services, or online reselling. Many entrepreneurs use this amount as startup capital.

However, in urban areas with high rent, school fees, and family responsibilities, ₦1 million can be used up quickly if not managed properly.

So, while ₦1 million is a lot in terms of opportunity and financial potential, its true value depends on financial discipline, budgeting, and spending habits. Managed well, it can create wealth. Mismanaged, it can disappear quickly.

What’s the lowest salary in Nigeria?

The lowest salary in Nigeria is not strictly fixed nationwide because it depends on employment type, sector, and location. However, the national minimum wage in Nigeria is ₦70,000 per month (recently reviewed and adopted in many states and federal structures). This figure is meant to be the legal baseline for formal workers in government and organized private sectors.

Despite this, many informal or casual workers still earn less than the official minimum wage. For example, domestic workers, apprentices, or part-time laborers may earn between ₦20,000 to ₦60,000 monthly, depending on the arrangement. Some internships or entry-level informal jobs may even be unpaid or offer stipends below ₦50,000.

It’s also important to understand that the “lowest salary” is heavily influenced by cost of living. In rural areas, wages tend to be lower but expenses are also lower. In urban areas like Lagos or Abuja, even the minimum wage may not fully cover basic living costs due to higher rent and transport expenses.

So, while ₦70,000 is the official benchmark, real earnings across Nigeria vary widely. This is why many people rely on side hustles or additional income sources to survive or improve their financial situation.

How to budget a monthly salary?

Budgeting a monthly salary is about planning how every part of your income will be used before you spend it. The first step is to determine your total monthly income, including salary and any side income. This gives you a clear financial starting point.

Next, list your essential expenses, such as rent, food, transport, electricity, and internet. These must always be prioritized because they cover your basic survival needs.

After that, allocate money for savings and emergency funds. Even if it is small, consistency is more important than amount. Saving helps you prepare for unexpected situations.

Then, set aside money for debt repayment if you have loans or obligations. Clearing debt reduces financial pressure over time.

Finally, allocate a portion for wants and lifestyle spending, such as entertainment, shopping, or eating out. This ensures balance so you don’t feel restricted.

A popular structure is the 50/30/20 rule, but you can adjust it depending on your income level. The most important principle is that every naira should have a purpose, and spending should be intentional, not random.

How to save 1k in 30 days?

Saving ₦1,000 in 30 days may seem small, but it is a good way to build discipline and consistency in money management. The easiest method is to break it down into daily or weekly targets.

To save ₦1,000 in 30 days, you only need to save about ₦34 per day. This can be done by reducing small daily expenses like snacks, airtime usage, or unnecessary transport costs.

Another method is the daily saving challenge, where you set aside ₦50–₦100 each day. Even saving ₦100 daily will give you ₦3,000 in a month, which exceeds your target.

You can also use a jar or digital savings app to store the money separately so you are not tempted to spend it.

Cutting one small habit, such as skipping one drink or snack per day, can easily help you reach this goal.

Although ₦1,000 is a small amount, the real purpose is not the money itself but building the habit of saving consistently. Over time, this discipline helps you manage larger financial goals.

What is the 5/20/30/40 rule?

The 5/20/30/40 rule is a budgeting method that divides income into four structured categories to help manage money more effectively. It is similar to other percentage-based budgeting systems but offers more detailed allocation.

The first 5% is usually set aside for charity, giving, or personal generosity. This encourages financial responsibility beyond personal needs.

The 20% portion is allocated to savings and investments. This helps build long-term financial security and wealth creation.

The 30% is often used for debt repayment or financial obligations. This ensures that loans and responsibilities are reduced over time.

The largest portion, 40%, goes to living expenses such as rent, food, transport, and utilities. This covers essential daily needs.

The strength of this rule is that it forces discipline by dividing income into clear purposes. However, it may need adjustment depending on income level and cost of living, especially in high-expense areas.

Overall, it promotes balanced financial planning by ensuring that income is not only spent but also saved, invested, and used responsibly.

What is the 3 6 9 rule of money?

The 3-6-9 rule of money is a financial safety guideline that focuses on building emergency savings based on months of expenses. It helps individuals prepare for financial uncertainty and income disruptions.

The first level, 3 months of expenses, is the minimum emergency fund. It is suitable for people with stable jobs or low financial risk. This helps cover short-term emergencies like job delays or unexpected bills.

The second level, 6 months of expenses, provides stronger financial security. It is ideal for freelancers, small business owners, or people with irregular income. It gives more time to recover from financial setbacks.

The third level, 9 months of expenses, offers maximum financial protection. It is recommended for individuals with high responsibilities or unstable income sources. It ensures long-term survival during financial crises.

The main purpose of this rule is to reduce dependence on loans or debt during emergencies. It also encourages disciplined saving habits and financial preparedness.

In simple terms, the 3-6-9 rule helps you build a financial cushion that protects you from uncertainty and gives you peace of mind.

What is the 70 20 10 budget?

The 70/20/10 budget is a simple money management system that divides your monthly income into three main parts to help you control spending and build financial stability. It is popular because it is easy to understand and apply, even for beginners.

The first part, 70%, is used for living expenses. This includes rent, food, transport, electricity, data, clothing, and other daily needs. It covers everything you need to survive and maintain your lifestyle.

The second part, 20%, is allocated to savings and investments. This is the portion that helps you build financial security over time. It can go into emergency savings, business investment, or long-term financial goals like buying land or building wealth.

The third part, 10%, is used for debt repayment, giving, or personal development. This may include paying off loans, supporting family, donating to charity, or learning new skills that can increase your earning power.

The main advantage of this system is balance. It ensures that you are not only spending on current needs but also preparing for the future and improving yourself financially.

However, in real life, the percentages can be adjusted depending on income level and cost of living. For example, someone with low income may need to spend more than 70% on needs and reduce savings temporarily. The goal is flexibility while maintaining discipline.

How to save money from salary?

Saving money from your salary requires discipline, planning, and consistency. The first step is to pay yourself first, which means setting aside savings immediately after you receive your salary before spending on anything else. This helps ensure that saving becomes a priority, not an afterthought.

Next, create a monthly budget that clearly separates needs, wants, and savings. Essential expenses like rent, food, and transport should come first, followed by savings, then lifestyle spending.

A very effective strategy is the automatic savings method, where a fixed amount is transferred directly into a savings account as soon as your salary is paid. This reduces temptation to spend the money.

You should also cut unnecessary expenses, such as impulse buying, frequent eating out, or unused subscriptions. Small daily leaks in spending can stop you from saving effectively.

Another important method is to set clear financial goals, such as saving for rent, emergencies, or business capital. Goals give direction and motivation to stay consistent.

Finally, track your spending throughout the month so you understand where your money goes. Awareness is key to improving financial habits.

By combining discipline, budgeting, and consistency, you can steadily save money from your salary regardless of your income level.