Many Nigerians experience a familiar struggle every month — the salary or income arrives, yet before the month ends, the money is already gone.

Bills are still waiting, food prices keep rising, transport costs increase without warning, and unexpected family needs appear at the worst time.

This creates financial pressure that leaves many people wondering how to survive the remaining days before the next income arrives.

The truth is that surviving financially before month-end is not only about how much you earn, but also about how you manage, prioritize, and stretch what you already have.

With the right mindset and simple practical strategies, it is possible to reduce financial stress, stay afloat, and regain control even in difficult economic conditions.

Understanding Why Money Runs Out Before Month-End

Many people in Nigeria find themselves wondering why their money disappears so quickly after receiving salary or income, and the answer is often a combination of habits, environment, and economic pressure rather than income alone. One major reason is poor budgeting habits.

A lot of people receive their money and start spending without a clear plan, leading to random purchases that do not align with essential needs.

When there is no structure guiding spending, money naturally slips away faster than expected.

Another common issue is impulsive spending right after salary alert. The excitement of receiving money after weeks of waiting can lead to unnecessary purchases such as new clothes, eating out, gadgets, or social activities that were not planned for.

While these expenses may seem small individually, they accumulate quickly and reduce available funds for the rest of the month.

Inflation also plays a serious role in financial strain. The cost of basic goods such as food, transport, and utilities continues to rise, meaning that the same amount of money now buys less than it used to.

This creates a situation where even carefully planned budgets become insufficient before the month ends.

Family responsibilities further increase financial pressure. Many individuals support parents, siblings, or extended relatives, which can lead to unexpected or recurring financial demands.

On top of that, transport fare fluctuations and daily living expenses in Nigeria can change without notice, making it difficult to stick to any fixed budget.

Finally, a lack of emergency planning worsens the situation. Without savings or a buffer for unexpected expenses like medical needs or urgent bills, people are forced to use their main income, causing it to run out faster.

Overall, it becomes clear that financial struggle before month-end is not just about low income but also about spending behavior, planning gaps, and economic realities.

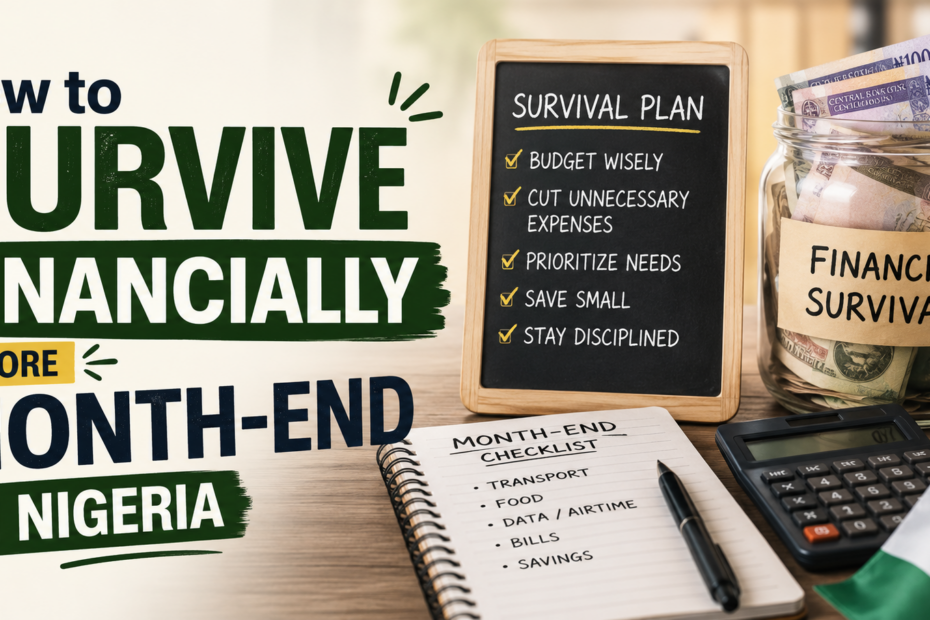

Prioritizing Survival Expenses Over Wants

One of the most important skills for surviving financially before month-end in Nigeria is learning how to clearly separate survival expenses from lifestyle wants.

When money becomes tight, every naira matters, and the way it is allocated can determine whether you will struggle or stay stable until the next income arrives.

Survival expenses are the basic things you cannot do without. These include rent or shelter-related costs, feeding, transport to work or school, essential communication like data or airtime for important contacts, and necessary medications or healthcare needs.

These are the expenses that keep life moving and ensure you can continue earning or functioning normally.

On the other hand, lifestyle wants are the things that improve comfort or enjoyment but are not immediately necessary for survival.

These include eating out frequently, buying new clothes when you already have usable ones, subscribing to multiple entertainment platforms, impulsive online shopping, or attending social events that require spending beyond your means.

While these things are not bad in themselves, they become harmful when money is already limited and survival is at risk.

At this stage, discipline becomes more important than desire. It requires making temporary sacrifices and accepting that comfort may need to be reduced until financial stability returns.

This might mean cooking at home instead of ordering food, reducing transportation costs by planning routes wisely, or pausing non-essential subscriptions.

It also means resisting social pressure that encourages spending just to “belong” or keep up appearances.

The goal is not to punish yourself, but to prioritize stability over pleasure in the short term. When survival needs are secured first, it becomes easier to manage stress and avoid debt or borrowing.

In this way, financial discipline becomes a protective tool that helps you stay afloat until your next income cycle.

Practical Strategies to Stretch Limited Money

When money is already tight before month-end, survival depends on how wisely you stretch what is left.

At this stage, the goal is not luxury or comfort but making every naira last as long as possible without creating additional financial pressure.

One of the most effective strategies is buying in smaller but smarter quantities. Instead of purchasing expensive bulk items that may finish your remaining funds at once, you can buy only what you need for a few days.

This helps you stay flexible while still managing essential needs like food and household items.

Another powerful approach is cooking at home instead of eating out. In Nigeria, eating from restaurants or ordering food frequently can drain money very quickly.

Preparing simple meals at home, even if they are basic, significantly reduces daily expenses and gives you more control over your spending.

It also allows you to plan meals around a fixed budget instead of reacting to hunger outside.

Transport costs can also be reduced with better planning. For example, combining errands into one trip instead of multiple movements can save money.

In some cases, walking short distances instead of taking transport for every movement can also help reduce daily expenses. While this may seem small, these small savings accumulate over time and make a difference.

Buying from bulk or local markets is another practical way to reduce spending. Local markets often offer cheaper prices compared to supermarkets, and buying directly from vendors can help you negotiate better deals, especially for food items.

Finally, a simple but powerful budgeting method is dividing your remaining money into daily allowances.

Instead of spending freely, you allocate a fixed amount for each day until the next income arrives. This prevents early exhaustion of funds and helps you maintain control over spending decisions.

Emergency Survival Habits That Help Mid-Month Crisis

When financial pressure becomes intense before month-end, having emergency survival habits can make a significant difference in how you manage the situation.

At this point, the focus shifts from normal budgeting to immediate problem-solving strategies that help you stay afloat without creating long-term financial damage.

One of the most important habits is borrowing only when absolutely necessary and doing so responsibly.

Borrowing should not become a lifestyle or a quick escape from poor planning. If it must be done, it should be from trusted sources such as family or friends, with a clear understanding of repayment to avoid strained relationships or ongoing debt cycles.

Another practical survival method is engaging in small side hustles to generate quick income.

In Nigeria, opportunities such as freelancing, small-scale reselling, food vending, or offering services like laundry, writing, design, or repairs can help bring in extra cash within a short period.

Even modest earnings from these activities can help cover essential needs like feeding or transport until the next income arrives.

Negotiating payment extensions is also a useful strategy that many people overlook. Some service providers or landlords may allow short delays if you communicate early and honestly about your situation.

This can help you avoid penalties or immediate financial pressure while giving you time to stabilize.

However, during financial stress, it is very important to avoid debt traps such as high-interest loans or quick online lending apps that often worsen financial problems.

While they may seem like a fast solution, they usually come with repayment terms that increase pressure in the following month, creating a cycle of continuous debt.

Ultimately, emergency survival habits are about finding balance—solving immediate needs without creating bigger problems for the future.

The goal is to stay stable, protect your financial reputation, and gradually regain control over your situation.

Building a System to Prevent Future Shortages

While surviving before month-end is important, the real long-term solution is building a system that prevents the problem from repeating itself.

Financial stability does not happen by accident; it is the result of consistent habits and intentional planning. One of the first steps is creating a monthly budget plan immediately after income is received.

Instead of spending randomly, you allocate specific portions of your money to key areas such as rent, feeding, transport, savings, and essential bills.

This structure gives your money direction and helps you avoid unnecessary depletion within the first few weeks.

Another powerful habit is gradually building an emergency fund, even if it starts very small. Saving a fixed amount from each income cycle creates a financial cushion that can support you during unexpected situations.

Over time, this emergency fund becomes a safety net that reduces the stress of mid-month financial crises and prevents reliance on borrowing.

Tracking daily expenses is also essential. Many people underestimate how small daily spending adds up over time.

By recording what you spend each day, you become more aware of your financial behavior and can quickly identify areas where money is being wasted.

This awareness naturally improves discipline and helps you make better spending decisions.

Beyond tools and methods, developing basic financial discipline is the foundation of long-term stability.

This includes delaying unnecessary purchases, avoiding emotional spending, and learning to prioritize needs consistently over wants. It also involves accepting that financial growth is gradual and requires patience.

Ultimately, building a financial system is about shifting from survival mode to stability. With consistency, what once felt like constant financial struggle can gradually turn into control, confidence, and peace of mind in your financial life.

Conclusion

Surviving financially before month-end in Nigeria is not about luck—it is about discipline, awareness, and intentional money management.

While the economy may be challenging and expenses may seem overwhelming, small consistent habits can make a big difference.

Learning to prioritize needs over wants, planning daily spending, reducing unnecessary costs, and finding legal side income opportunities can help you stay stable even when money is tight.

Most importantly, financial survival should not end at just “making it to month-end,” but should become a stepping stone toward better budgeting habits and long-term financial stability.

With patience and consistency, anyone can move from constant financial struggle to a more controlled and peaceful financial life.

Frequently Asked Questions

What is the 7 7 7 Rule for Money?

The 7 7 7 rule for money is a simple personal finance mindset strategy that helps people divide their income into balanced financial priorities so they can grow wealth while still enjoying life.

Although different versions exist, the most common interpretation breaks income into three parts: spending, saving, and investing in a structured percentage format that encourages discipline over impulse spending.

The idea is that money should not just be spent as it comes in, but intentionally directed toward stability and future growth.

In many practical uses, the rule suggests allocating around 70% of income for needs and lifestyle expenses, 20% for savings, and 10% for investments or financial growth opportunities.

The philosophy behind it is balance. Many people struggle financially not because they earn too little, but because they lack structure in managing what they earn.

By following a rule like this, even a small income can begin to build financial direction. The key benefit is consistency, because small savings and investments over time can grow into meaningful financial security.

How to Earn 5,000 Naira Per Day in Nigeria?

Earning 5,000 naira daily in Nigeria is realistic, but it depends on skill, consistency, and choosing the right income stream.

One of the most common ways is through small-scale digital services such as freelancing, writing, graphic design, or social media management.

Many beginners also earn this amount through buying and selling goods like food items, thrift clothing, or phone accessories with small profit margins.

The goal is not necessarily to find one big opportunity but to combine small daily earning activities that can reliably generate income.

Another strong approach is service-based work such as delivery services, tutoring, barbing, makeup, or laundry services.

These activities often bring daily cash flow because they solve immediate needs in your environment.

Even online opportunities like affiliate marketing or content creation can reach this level, but they require consistency and time before results become stable.

The key is to focus on one or two income streams and build them gradually rather than jumping between many ideas without structure.

What is the 3 6 9 Rule for Money?

The 3 6 9 rule for money is a financial discipline concept that focuses on time-based saving and investment consistency.

It is often used as a habit-building method rather than a strict financial formula. The idea is to develop strong money discipline by reviewing, saving, or investing money in cycles of 3 days, 6 days, and 9 days depending on personal goals.

This repetition builds awareness of spending behavior and encourages better control over financial decisions.

In practical application, some people use the rule to review expenses every 3 days, adjust budgeting every 6 days, and make savings or investment decisions every 9 days.

While it may not be a universal financial standard, it is useful for people who struggle with impulsive spending.

The repeated financial check-ins help individuals stay accountable and avoid unnecessary purchases. Over time, it builds a strong habit of financial awareness, which is more important than the rule itself.

How to Save Money Fast on a Low Income in Nigeria?

Saving money on a low income in Nigeria requires intentional discipline rather than high earnings. The first step is to separate savings immediately after receiving income, even if the amount is small.

This approach is known as “paying yourself first,” and it helps prevent the money from being spent on unnecessary needs. Even saving a small percentage consistently can create financial progress over time.

Another effective method is reducing lifestyle pressure. Many people struggle to save because they try to match a lifestyle that is above their income level.

Cutting down on unnecessary transport costs, eating out less, and avoiding impulsive online purchases can significantly increase savings capacity.

Using a simple budgeting structure where income is divided into essential needs, savings, and basic personal spending can also bring clarity and control.

Additionally, using savings tools such as cooperative contributions, thrift savings groups (ajo or esusu), or digital savings apps can help enforce discipline.

When money is locked or committed, it becomes harder to withdraw impulsively. The key is consistency, not the amount saved.

Over time, even small savings build financial security and open opportunities for investment or emergencies.

What is the 3 Rule Money?

The 3 rule money is a simplified financial guideline that focuses on controlling spending and building discipline with income management.

In most interpretations, it suggests dividing income into three main categories: essential needs, savings, and personal wants.

This helps individuals avoid financial imbalance where all income is spent without planning for the future.

The strength of the 3 rule lies in its simplicity. Unlike complex budgeting systems, it is easy to apply regardless of income level.

Essentials cover basic survival needs such as food, rent, and transport. Savings are set aside for emergencies or future goals, while the remaining portion is used for personal enjoyment.

This balance ensures that financial life is not only about survival but also about stability and mental satisfaction.

When consistently applied, the 3 rule helps reduce financial stress and builds long-term discipline. It teaches individuals to prioritize needs over wants and encourages the habit of saving even when income is small.

Over time, this simple structure can lead to better financial control and improved decision-making habits regarding money.

What are the 7 Pillars of Wealth?

The 7 pillars of wealth refer to the core foundations that support long-term financial stability and growth.

They are not a single formula but a combination of habits, skills, and systems that wealthy individuals consistently build over time.

These pillars often include earning income, saving, investing, financial education, multiple income streams, discipline, and asset ownership.

Each pillar works together to create a strong financial structure that can withstand economic challenges.

Income is the starting point because wealth cannot exist without money flowing in. However, saving ensures that a portion of income is preserved instead of being consumed.

Investing helps that saved money grow beyond inflation. Financial education is another critical pillar because it determines how well a person understands and manages money.

Multiple income streams reduce dependence on one source, while discipline ensures consistency in financial decisions.

Asset ownership, such as land, businesses, or investments, provides long-term security and generational wealth.

When these pillars are combined, they create a financial system that grows stronger over time instead of collapsing under pressure.

What are the 9 Words to Attract Money?

The idea of “9 words to attract money” is more motivational and mindset-based than a strict financial rule.

In most personal development teachings, it is often expressed as affirmations that shape how a person thinks about wealth.

A common interpretation is: “Money flows to me through multiple sources easily.” These words are designed to shift mindset from scarcity to abundance and encourage confidence in financial opportunities.

While affirmations alone do not generate income, they influence behavior, which is where real financial change happens.

When a person believes money is accessible and possible, they are more likely to seek opportunities, develop skills, and take action.

However, it is important to understand that money attraction is not magic; it requires effort, planning, and execution.

The value of such phrases lies in mental conditioning, helping individuals replace fear and doubt with a more proactive financial mindset that supports growth-oriented decisions.

What is the Golden Rule of Money?

The golden rule of money is a simple but powerful principle: spend less than you earn and invest the difference.

This rule is the foundation of all financial success because it ensures that a person is always building wealth instead of destroying it.

No matter how high or low income is, financial stability depends on controlling expenses and consistently saving or investing part of earnings.

Living by this rule requires discipline and awareness of lifestyle inflation. Many people increase their spending every time their income increases, which prevents them from building wealth.

The golden rule encourages resisting that temptation and instead directing extra income toward savings, investments, or business opportunities.

Over time, this creates financial freedom because money begins to work for the individual rather than being constantly spent on liabilities. It is simple in concept but powerful in real-life application.

What is the Rule of 72 in Money?

The Rule of 72 is a financial formula used to estimate how long it will take for an investment to double in value based on a fixed annual interest rate.

The formula is simple: divide 72 by the interest rate to get the approximate number of years it will take for money to double. For example, if an investment earns 12% annually, it will take about 6 years for the money to double.

This rule is widely used in investment planning because it helps people understand the power of compound interest.

It shows how even small differences in interest rates can significantly affect long-term growth.

The Rule of 72 is not perfectly exact, but it is highly practical for quick financial estimation. It encourages long-term thinking and helps investors choose better financial opportunities by comparing returns across different investment options.

How to Make 2K Daily in Nigeria?

Making 2,000 naira daily in Nigeria is achievable through consistent small-scale income activities, especially when combined strategically.

One of the most accessible methods is buying and selling everyday items such as snacks, water, mobile accessories, or thrift clothing.

These items move quickly in busy environments like schools, motor parks, and marketplaces, allowing steady daily profit margins.

Another effective approach is service-based work such as laundry, barbing, hairdressing, or small delivery services. These services generate daily cash flow because they solve immediate needs in the community.

Digital opportunities also exist, such as mini freelancing tasks, social media management for small businesses, or affiliate marketing, although these may take time to stabilize. The key is consistency and focusing on activities that have daily demand.

The most important factor is not just choosing an idea but sticking to it long enough to understand how it works in your environment.

Many people struggle not because opportunities are absent, but because they switch too quickly between ideas. With discipline and repetition, even small daily earnings can become stable income over time.

How to Make 1K Per Day?

Making 1,000 naira per day in Nigeria is one of the most realistic entry-level income goals, especially for beginners who are trying to build financial stability.

The key idea is not to look for one big opportunity but to combine small, consistent earning activities that reliably generate daily cash flow.

At this level, what matters most is consistency, location, and understanding what people around you already spend money on every day.

One of the easiest ways is through micro trading. This includes selling items like sachet water, snacks, fruits, recharge cards, or small household essentials in busy areas such as bus stops, schools, or residential neighborhoods.

Even with a small capital, a slight profit margin on each item can quickly add up to 1,000 naira or more per day.

Another practical approach is offering small services like helping people run errands, washing clothes, cleaning, or assisting local shop owners.

These services may look small, but they are always in demand and can generate daily income if you remain consistent.

Digital opportunities also exist, especially for people with smartphones. Simple tasks like data entry, posting content for small businesses, WhatsApp marketing, or basic freelancing gigs can help you reach this target.

The important thing is to treat 1,000 naira per day not as the final goal but as a starting foundation. When consistency is built, it becomes easier to scale into higher daily income levels.

How to Earn 5K in 1 Hour?

Earning 5,000 naira in one hour is possible, but it is not something that happens passively or randomly. It usually comes from either high-demand skills, urgent services, or selling high-margin products.

The reality is that time alone does not create money; value does. The more valuable and urgent your service or product is, the more likely you are to earn that amount quickly.

One of the most realistic ways is through skill-based services such as graphics design, website fixes, phone repairs, or makeup and hairstyling for events.

These services often have urgent demand, especially when clients are preparing for events or deadlines.

Another strong method is flipping products—buying and reselling items like gadgets, shoes, or accessories where profit margins are higher per sale. In some cases, one successful sale can generate 5,000 naira or more within a short period.

However, it is important to be realistic. For beginners without skills or setup, earning 5,000 naira in one hour is not consistent.

It usually requires preparation, experience, and a strong network of clients or buyers. The real strategy is to first build skills or a small business system that positions you where high-paying opportunities come quickly when demand arises.

What Creates 90% of Millionaires?

Most studies on wealth creation consistently show that the majority of millionaires are not created through sudden luck but through entrepreneurship, investment, discipline, and long-term asset building.

A large percentage of wealthy individuals build their wealth through business ownership, where income is not limited to a fixed salary but scales with effort, systems, and market demand. Business allows wealth to grow exponentially compared to regular employment.

Investments also play a major role, especially in real estate, stocks, and long-term financial assets. Many millionaires accumulate wealth over decades by consistently investing part of their income instead of spending everything.

Another major factor is financial discipline, which includes living below their means, avoiding unnecessary debt, and focusing on asset accumulation rather than liabilities.

It is also important to understand that inheritance and generational wealth contribute to a portion of millionaires globally, but the majority still build wealth over time.

The key pattern across most wealthy individuals is not just income, but how income is managed, multiplied, and preserved.

Wealth creation is therefore less about how much a person earns and more about how consistently they convert income into assets.

What is the 777 Rule for Money?

The 777 rule for money is a financial discipline concept often used in personal finance education and mindset training.

While it does not have one fixed definition, it is commonly understood as a structured way of managing money through repeated cycles of saving, investing, and reviewing financial decisions.

In some interpretations, it refers to dividing attention across financial goals in a disciplined pattern that reinforces consistency over time.

A common version of the idea encourages individuals to consistently check, save, or adjust their finances in repeated cycles, helping them stay aware of their spending habits.

The goal is to build strong money awareness and avoid impulsive financial behavior. It is less about mathematics and more about behavioral discipline, ensuring that money decisions are intentional rather than emotional.

The value of the 777 rule lies in repetition and awareness. Many people struggle financially not because they do not earn enough, but because they do not track or control how money moves in and out.

By applying structured habits like this, individuals begin to develop financial discipline, which is one of the strongest foundations for long-term stability and wealth building.

Who is the 95-Year-Old Billionaire?

The “95-year-old billionaire” commonly refers to Warren Buffett, one of the most successful investors in history.

He is widely known for leading Berkshire Hathaway and building his fortune through long-term value investing rather than speculation or short-term trading.

His approach to wealth is centered on patience, discipline, and buying strong businesses at fair prices, then holding them for many years.

Buffett’s wealth journey is a powerful example of compounding and long-term thinking. Instead of chasing quick profits, he focused on consistent growth over decades, allowing small gains to multiply significantly over time.

He is also known for living modestly compared to his wealth level, showing that financial discipline plays a major role in sustaining wealth.

His success highlights an important financial lesson: wealth is not only about making money but about time, patience, and smart decision-making.

Many investors study his principles because they demonstrate that long-term consistency often outperforms risky short-term strategies.

What Are 7 Sources of Income?

The idea of having multiple sources of income is one of the strongest financial principles for long-term stability and wealth building.

A single income stream, such as salary or business profit, can be risky because it depends entirely on one channel.

When that source is disrupted, financial pressure becomes immediate. That is why financially stable individuals often diversify how money comes into their lives.

Common sources of income include active income from jobs, business income from self-employment or entrepreneurship, investment income from assets like stocks or real estate, and passive income from digital products or royalties.

Others include freelance or skill-based income, commission-based earnings such as sales or affiliate marketing, and side income from small trading or gig work.

Each of these income streams behaves differently, but together they create financial balance and reduce dependency on one source.

The key advantage of multiple income sources is resilience. For example, someone earning from a job but also running a small business or earning from investments is less likely to experience total financial breakdown during economic challenges.

Over time, the goal is to shift from purely active income—where time is directly exchanged for money—to more scalable or passive forms of income that continue even when you are not actively working.

Wealthy individuals often focus on building systems that generate money continuously rather than relying on constant effort alone.

Can ChatGPT Make Me Money?

ChatGPT can support you in making money, but it cannot directly generate income on its own. It is a tool, not a money source.

Its value depends entirely on how you use it. Many people now use AI tools like ChatGPT to speed up work, create content, learn skills faster, and improve productivity, which indirectly leads to income opportunities.

For example, someone can use it to write blog posts, create business ideas, draft marketing content, or learn freelancing skills more quickly.

In practical terms, ChatGPT can help you start online businesses faster. You can use it to write product descriptions, generate social media content, build business plans, or even learn how to code or design.

This reduces the learning curve and helps beginners enter digital income spaces like freelancing, affiliate marketing, or content creation.

However, the tool does not replace action. Without execution, the ideas and content it generates have no financial value.

It is also important to avoid unrealistic expectations. ChatGPT is not a “get rich quick” solution. Instead, it is a productivity multiplier.

People who combine it with real skills, consistency, and market understanding are the ones who benefit financially.

In simple terms, ChatGPT can help you make money faster, but only if you are already willing to work, learn, and apply what it helps you create.

How to Earn 100K in a Day?

Earning 100,000 naira in a single day is possible, but it is not common for beginners and usually requires either high-value skills, strong business systems, or large-scale trading.

At this level, income is no longer about small daily hustle but about value creation, timing, and market access. The higher the income target, the more important specialization and positioning become.

One realistic way to reach this level is through high-demand services such as event planning, large catering jobs, digital marketing campaigns, or tech services like website development.

In these cases, a single client payment can reach or exceed 100,000 naira depending on the project size.

Another approach is product-based business, where bulk sales or high-margin items are moved quickly, especially during peak demand periods.

It is also important to understand that such income levels often come from experience and reputation.

People who consistently earn this amount usually have built trust, networks, and systems that bring high-paying clients.

For beginners, the realistic path is to first build smaller consistent income streams, then scale skills or businesses over time until larger earnings become natural outcomes rather than forced goals.

Who Is the Dumbest Billionaire?

It is not accurate or fair to label any billionaire as the “dumbest,” because reaching billionaire status requires significant intelligence in at least one area such as business strategy, timing, innovation, or risk management.

Wealth at that level is rarely accidental, and even billionaires who make controversial decisions often demonstrate strong abilities in other areas that contributed to their success.

For example, well-known billionaires like Elon Musk and Jeff Bezos have both faced criticism for business decisions, yet they are also responsible for building companies that transformed global industries.

Similarly, Warren Buffett is widely respected for his disciplined investment approach, showing that success comes in different forms depending on strategy and field.

Instead of focusing on “dumbest” labels, a more useful approach is to study both successes and mistakes of wealthy individuals.

Billionaires are human and can make errors, but their overall success comes from repeated decision-making in complex environments.

Learning from their strategies, both good and bad, is far more valuable than judging them. Wealth creation is better understood through patterns of discipline, risk-taking, and long-term thinking rather than simplified labels.

How to Stay Rich Forever?

Staying rich is often more difficult than becoming rich because maintaining wealth requires discipline, planning, and emotional control.

Many people lose money not because they do not earn enough, but because they fail to manage it properly after they start making more. The foundation of lasting wealth is financial discipline, especially the ability to control lifestyle inflation.

One of the most important principles is living below your means regardless of income level. When income increases, expenses should not increase at the same rate.

Instead, extra income should be directed toward investments, savings, or asset building. Wealth is preserved when money is consistently converted into income-generating assets rather than consumable liabilities.

Another important factor is diversification. Wealthy individuals rarely depend on one income source or one investment type.

They spread risk across businesses, investments, and financial instruments to protect themselves from market changes.

Long-term thinking is also critical. People who stay rich focus on decades, not days, and prioritize stability over short-term luxury.

Ultimately, staying rich is less about how much money you make and more about how you behave with money over time. Consistency, discipline, and patience are what separate temporary wealth from lasting financial freedom.